How to Combine Finances After Marriage

My husband and I got married a few years ago. We are both CFP® professionals. Between the two of us, we have years of experience helping couples talk through exactly this kind of thing.

And still when it came to our own finances, we had to actually sit down and figure it out. There is no clear right or wrong answer.

What accounts would we combine? What would stay separate? Who would manage what bills? What does “fair” even mean when two people with different financial histories decide to build a life together?

I tell that story because I want you to hear this: if you haven’t figured this out yet, you’re not behind. Most couples haven’t. And there is genuinely no single right answer. What matters is that you pick a system that you both understand and feel good about.

Here’s how to think through it.

Why “Combine Finances” Feels So Complicated After Marriage

When you combine finances after marriage, it doesn’t feel difficult because of math. It’s because money is so deeply personal. You each come into the marriage with your own history, your own habits, your own relationship with spending and saving, your own sense of what financial security feels like.

Then suddenly you’re sharing a life, and possibly sharing accounts, with another person. It can feel vulnerable. It can bring up questions you’ve never had to answer before: What if we disagree on a purchase? What if one of us earns more? What if I want some financial independence?

Those feelings are normal. And they’re exactly why the conversation matters. Not so you can arrive at the “correct” answer, but so you can arrive at your answer, together.

“Most couples don’t avoid this conversation because they’re irresponsible. They avoid it because they’re not sure how to start it and they’re afraid of saying the wrong thing.”

The three ways couples combine finances after marriage

When I sit down with newlyweds, I walk them through three common approaches. None is universally better. Each has real tradeoffs depending on how you and your partner are wired.

Fully combined

All income flows into shared accounts. Every bill, savings goal, and purchase comes

from the same place. Nothing is “mine”. It’s all “ours.”

| Pros | Cons |

|---|---|

| Total transparency | Less personal autonomy |

| Simple to manage | Every purchase is visible, which can create friction if spending styles differ significantly |

| Naturally keeps both partners aligned on spending and saving | Requires strong communication and trust to avoid conflict |

Best for: Couples who value full transparency and think of every financial decision as a team effort.

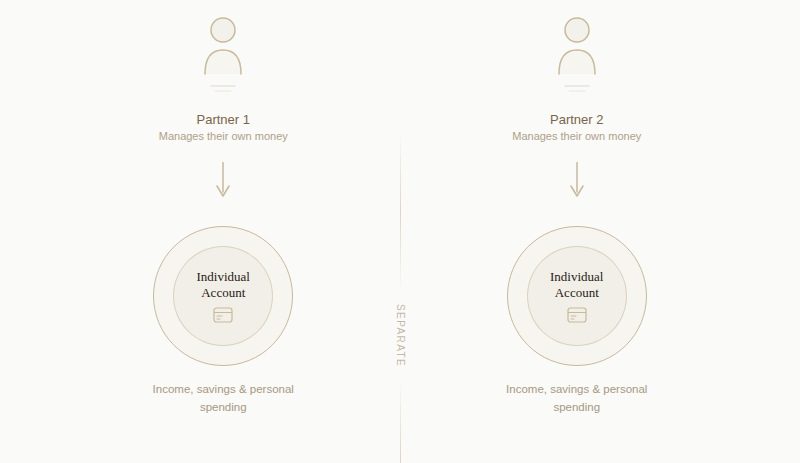

Separate, but coordinated

Each person keeps individual accounts. Shared expenses such as rent, groceries, utilities are split either equally or proportionally by income.

| Pros | Cons |

|---|---|

| Full control over your own money | Shared goals can slip through the cracks, they belong to neither account |

| Income differences are easier to navigate on your own terms | Can start to feel transactional over time, like splitting a bill with a roommate |

| Limits friction if your saving and spending styles are very different | Easy to lose visibility into the full financial picture as a unit |

Best for: Couples who genuinely value independence or whose financial starting points look very different.

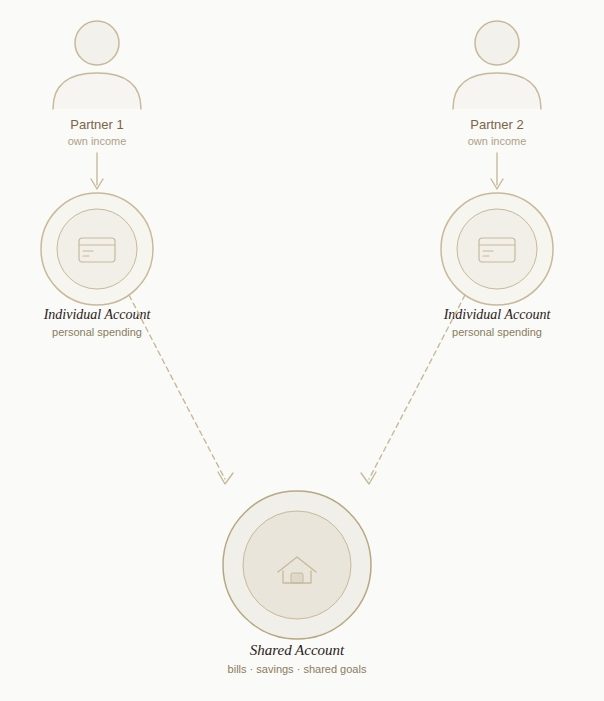

Hybrid Approach

A joint account for shared expenses and goals. Individual accounts for personal spending.

| Pros | Cons |

|---|---|

| Shared clarity on what matters most without giving up personal autonomy | Requires an upfront agreement on how much each person contributes |

| Personal spending stays personal, No narrating every small decision | More accounts to track. The system can quietly fall apart without some organization |

| Flexible and easy to adjust as income or priorities change | Financial stress can hide in a personal account and delay conversations you need to have |

Best for: Couples who want alignment on the big picture but room to breathe on the small stuff.

Before You combine your finances: Questions to talk through with your partner

Before you open any accounts or make any decisions, have the conversation first. These questions are designed to surface what you each actually think.

Your money history

- Growing up, how did your family talk about money?

- Are you more of a spender or a saver by nature? Has that ever caused stress for you?

- What does financial security feel like to you? What does it take for you to feel “okay”?

- Have you ever been in a situation where money felt really tight? How did that shape you?

How you’ll manage money together

- Does the idea of combining all our accounts feel freeing or uncomfortable and why?

- Is there a spending amount where you’d want to check in with each other before buying?

- Who will handle the day-to-day bills and account management, or will we share that?

- What would feel like a “financial win” for us this first year?

What “fair” means to you

- If our incomes are different, should we split shared expenses equally or proportionally?

- Should we each have personal spending money that’s ours without needing to explain it?

- How do you want to handle it if one of us loses a job, goes back to school, or takes time off for family?

The big picture

- What are the two or three financial goals that matter most to you in the next five years?

- What would it mean to you to feel financially “on track” as a couple?

- Is there anything about money that you’ve been nervous to bring up that we should probably talk about?

You don’t have to answer all of these in one sitting. Some couples work through them over a few conversations. The goal isn’t to resolve everything. It’s to understand each other well enough to build something that actually fits.

Exercise: Choose What Matters Most

For each pair, individually choose the option that feels most like you. Don’t overthink it. Go with your instinct.

Lifestyle Now <──────────────> Future Wealth

I want to enjoy a higher quality of life now, even if it means saving less

I want to prioritize saving and investing now, even if it means sacrificing lifestyle

Security <──────────────> Flexibility

I want to feel financially secure and avoid stress about money

I want flexibility to take risks or make big life/career changes

Home <──────────────> Freedom

I want to buy a home as a top priority

I’d rather keep flexibility to travel/move over owning a home.

Experiences <──────────────> Long-Term Goals

I want to spend more on travel and experiences now

I want to focus more on long-term goals like retirement or wealth-building

Legacy <──────────────> Personal Lifestyle

I want to build wealth to leave behind for future generations

I want to prioritize our lifestyle and experiences during our lifetime

Now the important part

Compare your answers and talk through:

- Where did we choose the same thing?

- Where did we choose differently?

- Which differences feel easy vs. harder to reconcile?

- What would a “middle ground” look like for us?

How to get started: combine your Finances

Most couples don’t struggle with understanding what to do. They struggle with knowing where to begin. Here’s a simple sequence that works.

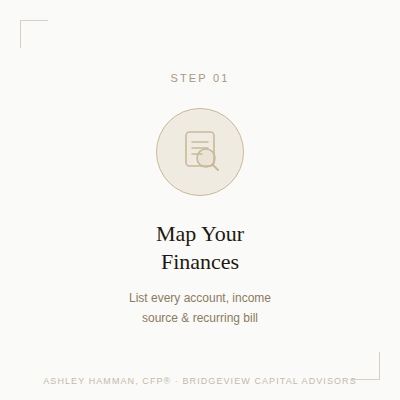

Step 1 — Map your current financial picture together List every account, every income source, every recurring bill. You can’t build a shared system until you both know what you’re working with.

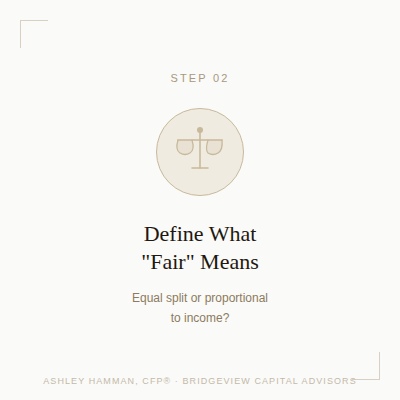

Step 2 — Decide what “fair” means for your household Fair doesn’t always mean equal. If one partner earns more, a proportional split may feel more balanced than 50/50. Talk about it before you set anything up.

Step 3 — Choose your structure, then open the accounts Pick one of the three approaches above. Open whatever new accounts you need. Keep it simple to start you can always adjust as your life changes.

Step 4 — Build your shared goals into the plan A home, travel, kids, an emergency fund. Your financial structure should actively work toward the life you’re building together. Connect your accounts to your actual goals, not just your monthly bills.

Step 5 — Put a regular check-in on the calendar Monthly or quarterly, 20 minutes, low pressure. Couples who talk about money regularly make better decisions and argue about it less.

Money & Marriage: A newlywed Guide

I put together a free guide specifically for newlyweds. it covers how to combine finances, what changes after marriage, tax and benefit basics, community property in California, and a simple 8-step checklist to get organized in your first year together. If you’re newly married or about to be, it’s a calm and practical place to begin.

What’s inside:

- The 8-Step Money & Marriage Checklist

- What Actually Changes Financially When You Get Married

- How to Combine Your Finances

- Tax and Insurance Updates to Make Right Away

- Understanding Community Property in California

- When it Makes Sense to Work with a CFP®

California & Community Property States

California is a community property state (along with Arizona, Nevada, Texas, Washington, and a few others). What that means in practice: most income earned during the marriage is legally owned equally by both spouses, regardless of who earned it. Most debts taken on during the marriage are shared too, even if only one name is on the account.

This doesn’t mean you have to combine everything. But it does mean that how you title accounts (and how you keep pre-marital assets separate) is crucial. If you’re bringing significant savings or investments into the marriage, it’s worth a conversation with a professional on how to protect what’s yours individually.

Frequently Asked Questions

Not necessarily, but many couples benefit from at least one joint account for shared expenses. Whether you go fully combined, fully separate, or somewhere in between depends on your goals, income levels, and what feels fair. What matters most is that you’ve both agreed on the structure and actually understand how it works.

Sometimes people use a proportional contribution model, where each person puts in the same percentage of their income toward shared expenses. But some couples prefer fully combined, treating all income as shared regardless of source. Talk about what feels sustainable to both of you before you set anything up.

In most cases, debt you had before the wedding stays yours individually. But debt taken on after the marriage, especially in community property states like California, can be considered shared, even if only one name is on the account. This is worth understanding early, especially if one of you is carrying significant student loans or credit card balances.

That’s actually normal and it’s exactly why the priority exercise above exists. Disagreement isn’t a red flag. It’s information. The goal isn’t to have identical financial personalities. It’s to understand where you’re different and build a plan that accounts for both of you.

No. Plenty of couples work this out on their own. But a CFP® professional can help you think through the details more intentionally: taxes after marriage, coordinating retirement accounts, reviewing insurance, and building a plan around your shared goals. Think of it less as needing help and more as choosing to start strong.

The bottom Line

There is no perfect way to combine finances after marriage. There is only the way that works for you, the one you’ve both agreed on, that you understand, and that gives you a clear system for managing money as a team.

What trips couples up isn’t choosing the wrong structure. It’s not choosing at all. That is a decision on it’s own. You don’t have to have it all figured out before you start. You just need to start.