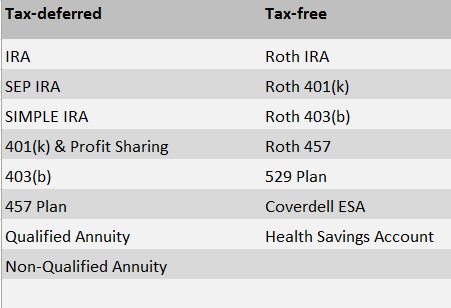

Tax-deferred vs Tax-free is a concept that is key to making good financial planning decisions. Most retirement accounts fall into these two categories. It’s critical to know which ones are which. It is also worth noting, this concept applies to more than just retirement accounts. Choosing which investment account to use for health and education planning requires a solid understanding of tax-deferred vs tax-free as well.

Tax-deferred vs Tax-free Investment Accounts: Tax-deferred basics

This method of taxation means you’ll pay the taxes later. In an effort to encourage individuals to save for their retirement, the government provides this tax incentive.

Funds you contribute to a retirement account won’t be taxed until you withdraw the funds. The most common type of retirement accounts with this feature are IRAs, SIMPLE IRAs, 401(k)s, 403(b)s and 457 plans.

There are two main concepts that make this attractive.

First, shielding funds from capital gains and dividend taxes will allow more of the funds to remain invested. This increases the effect of compounding returns. The greater the number of years until retirement, the greater the benefit of the tax deferral. This is yet another reason to start saving early.

Second, when you withdraw funds during retirement, you’ll owe less in taxes on the distribution. This assumes you’re in a lower tax bracket during retirement than you were when you originally made the contribution.

Tax-deferred is not to be confused with tax-deductible. When you invest in a Traditional IRA, the assumption is that you deducted the contributions from income. As a result, withdrawals from Traditional IRAs are 100% taxable as income (contributions and earnings). The rationale for this is that those funds were never taxed.

For example, one could make a contribution to an IRA and not be allowed the tax-deduction. If you didn’t deduct the contributions from your taxable income, you made a “non-deductible” IRA contribution. However, you would still receive the tax-deferred status on the investment’s earnings from capital gains and dividends. It should be noted that taking a deduction from income or reducing your salary through a 401(k) or 403(b) will give you the biggest bang for your buck.

Tax-deferred vs Tax-free Investment Accounts: Tax-free basics

Probably the least understood and most under-utilized form of taxation for retirement accounts is the tax-free method. This form of taxation allows one to make contributions to a retirement account and receive the same benefits of tax-deferred accounts while the money is invested.

Most notably, these accounts are Roth IRAs and 401(k) and 403(b) plans with Roth features (tax-free). However, there is one huge difference. With a tax-free account, you pay NO taxes when the funds are taken out during retirement. This is in contrast to a tax-deferred account where you pay income tax on whatever you spend from the account.

The key point to understand about tax-free accounts is that they don’t offer an immediate tax benefit like deductible IRA contributions and salary contributions to a 401(k), 403(b), or SIMPLE IRA plan.

With these tax-deferred plans, you are reducing your income tax liability for the year in which the contributions are made, thus reducing your tax bill. With tax-free accounts like Roth IRAs and company retirement plans with Roth features, contributions are made “after tax” so you don’t get an immediate income tax savings.

To make matters a little more complicated, company retirement plans with Roth features (tax-free) will have a combination of tax-deferred AND tax-free. This occurs because a 401(k) that pays matching and/or profit sharing contributions is doing so under the tax-deferred method.

More about Roth IRAs:

It is important to note that Roth IRA contribution limits are based on Modified Adjusted Gross Income or MAGI. If you discover that you made a contribution but weren’t eligible, you will need to contact your investment provider. They will need to process either an “excess withdrawal” or a “re-characterization.”

An excess withdrawal removes from the Roth IRA what you over contributed.

The re-characterization will change it from a Roth contribution to a Traditional IRA contribution. In this scenario, you will have moved funds from tax-free status to tax-deferred.

There is also what is known as a “Back Door Roth IRA Contribution.” This is where you make a contribution to a non-deductible IRA and then convert it to a Roth IRA. This can be a tricky process. I wrote about some of the pitfalls in an article called Roth IRA Conversion – The Pro Rata Rule Is Lurking which goes into a little more detail.

Five-year waiting rule for Roth IRAs

The five-year waiting rule for Roth IRAs applies in two situations:

- In order to receive a qualified distribution of earnings (not principal) tax-free, the withdrawal must not be within 5 years of the date of the first contribution. These time periods are governed by the beginning of the tax year for which the contribution applies as opposed to the actual date.

- In order to receive a qualified distribution from a Roth IRA that was converted from an IRA without penalties applied to principal, the withdrawal must not be within 5 years of the date of the conversion.

Tax-deferred vs Tax-free isn’t just for retirement accounts

Education Saving

If you are specifically planning and saving for future college expenses, a 529 plan is built specially for this. Future withdrawals from the 529 will be tax-free if they are used on qualified education expenses. In addition, while the funds are invested in the account they aren’t subject to tax either. In ordinary investment accounts, earnings like dividends and realized capital gains are subject to taxes. You should be aware that if the funds aren’t used for qualified education expenses, the amount attributable to earnings will be subject to taxes and penalties.

If you are looking to save for educations expenses prior to college, a Coverdell ESA may be a better fit. I write about Coverdell ESAs in more detail in the article Is A Coverdell ESA Right For You?

Both Coverdell ESA and 529 plans are very similar to the the taxation of Roth IRAs.

Health Savings Account: The tax benefits of HSA Plans

HSAs provide a powerful incentive for use due to unique tax benefits because they allow a tax deduction on the front end and are tax free upon withdrawal. Contributions made to an HSA are tax deductible. If an employer makes contributions on your behalf, those contributions are excluded from your taxable income. If you make the contributions, they are a deduction. Interest and other earnings on your investment are tax exempt. That means no 1099 at the end of the year like a traditional investment account. Lastly, withdrawals made to cover qualified healthcare expenses can be made tax free!

Tax-Deferred vs Tax-Free Investment Accounts FAQ

ax-deferred means you postpone paying taxes on investment earnings until you withdraw the funds, usually in retirement. This allows your money to grow faster since it’s not reduced by annual taxes on gains and dividends. Common tax-deferred accounts include Traditional IRAs, 401(k)s, 403(b)s, and 457 plans.

Traditional IRAs are tax-deferred—you pay taxes when you withdraw the money. Roth IRAs are tax-free—you pay taxes on contributions upfront but owe nothing on qualified withdrawals. This makes Roth IRAs ideal if you expect to be in a higher tax bracket in retirement.

The five-year rule states that Roth IRA earnings can only be withdrawn tax-free if at least five years have passed since your first contribution. The rule also applies to Roth conversions to avoid penalties on early withdrawals.

High earners can use a “Backdoor Roth IRA” strategy—contributing to a non-deductible Traditional IRA and then converting it to a Roth IRA. However, this process can be complex due to the IRS pro-rata rule, so professional guidance is recommended.

HSAs offer triple tax benefits: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. They combine the best of both tax-deferred and tax-free strategies.

Tax-deferred and tax-free are both important components of a strong financial foundation. Understanding these concepts will result in better decisions about your retirement now and into the future.

Have you considered how a Certified Financial Planner™ can help you?

5 Comments

Comments are closed.