We hear a lot about the need for diversification when talking about our investments. You know the expression “don’t put all your eggs in one basket.” In the investment world this most often refers to the idea that you shouldn’t put all of your investment in one stock. But what about taxes when planning for retirement?

Without careful planning, you could end up in a higher tax bracket and pay more income tax than necessary. Working with a Certified Financial Planner™ for guidance on your specific situation can help reduce taxes in retirement.

The OBBBA increased the standard deduction for seniors

The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, introduced significant changes to how retirees are taxed most notably through an increased standard deduction for seniors. This change was designed to provide meaningful tax relief and reduce the overall income tax burden for older Americans living on fixed or limited retirement income.

Base standard deduction (2025):

- $15,750 for single filers

- $23,625 for heads of household

- $31,500 for married couples filing jointly

Additional senior deduction:

- $2,000 for single or head of household filers aged 65+

- $1,600 for each spouse aged 65+ if filing jointly

New temporary “bonus” deduction for seniors:

Seniors aged 65 and older can claim an extra $6,000 per individual ($12,000 for a couple where both spouses are 65+). This temporary bonus applies from 2025 through 2028 and phases out for higher-income taxpayers.

For more details about who qualifies un the OBBBA, grab the FREE guide linked below.

Now let’s explore how we pay taxes on various investment accounts and the concept of tax diversification.

Tax-Deferred Retirement Accounts

Typically, most retirement accounts are funded with pre-tax dollars. For example, when you contribute to a 401k or 403b plan, your contributions reduce your taxable income. This is the pre-tax part. Your money is contributed to the account “before” it has been taxed. This includes contributions to a Traditional IRA.

While those funds are invested, they are not subject to tax that would ordinarily apply to non-retirement accounts. However, during retirement when you withdraw money, you will pay ordinary income tax. This is the “deferred” part. You were able to “defer” tax while it was invested but must pay once you begin spending in retirement.

What most people forget is that when it comes time to fund your retirement, the withdrawals from these accounts are taxed as ordinary income. Simply put, it’s like receiving a paycheck. Uncle Sam will want his cut and who knows where tax rates might be in 30 years.

Tax-Free Accounts

Withdrawals from a Roth IRA are tax free! This type of retirement account is funded with after tax dollars (from your checking account) so when you retire you can make tax-free withdrawals.

Some employers allow Roth contributions in your 401 k or 403 b at work. In this case, you contribute funds after-tax. You don’t receive a reduction in your taxable income, but unlike tax-deferred, Roth IRA withdrawals are not considered ordinary income.

Roth IRA withdrawals of principal are tax and penalty free. The reason is that contributions are made with after tax dollars. The IRS has already taken their bite regarding the principal (what you contributed).

The earnings are a different story. While there can be exceptions, early withdrawals can be subject to taxes and penalties that are attributable to earnings (not principal).

Early withdrawals are those made prior to age 59 ½. Withdrawals made after age 59 ½ and after having the account for at least five years will allow for withdrawals that are tax and penalty free.

Taxable Investment Accounts

A taxable account isn’t given special tax treatment like retirement accounts. However, that doesn’t mean they should be ignored.

These are funded with after tax income. Interest and dividends generated by the investments are reported on a 1099 each year and must be reported to the IRS. If you sell an investment, you may be subject to capital gains tax if it increased in value.

Depending on how long you held the investment you would be subject to long term capital gains or short-term capital gains. It’s important to note capital gains tax rates are usually less than income tax rates. Additionally, you could use an account like this to reduce taxes by selling some securities for a loss.

Don’t Get Into The Prediction Business

A healthy and well diversified retirement savings will include all three categories. They will give you more choices and allow you to minimize taxes.

There is always talk of tax reform and potentially lower tax rates. I would be very cautious about holding off on the Roth IRA due to potentially lower tax rates.

It isn’t a sure thing that your taxes will be lowered even if there is tax reform. If your rates are reduced now, it is possible that tax rates could rise in the future. It is impossible to know what the future will hold. Because of that, it would be prudent to set aside funds that could be used tax-free many years down the road.

I’m often asked which is better, tax-free or tax-deferred. Answering this question requires a crystal ball or the ability to predict whether taxes will be higher or lower in the future. While there are compelling arguments to be made that taxes will be higher in the future, there is no way to know for sure.

Here is a more complete list of tax-deferred vs. tax-free accounts.

Mutual Funds In Taxable Accounts

Mutual funds are not tax efficient investments. When the portfolio manager of mutual fund buys and sells securities, they pass those gains on to shareholders of the fund. This is known as a capital gain distribution. Even though you didn’t sell your investment for a gain, you still pay capital gains tax.

While this isn’t much of a problem when they’re are held in retirement accounts, it can be when held in a taxable account. In some cases, you can even be hit with a capital gains distribution when you have unrealized losses. That’s brutal!

Exchange Traded Funds or ETFs are more tax efficient and may be a better fit for non-retirement investment accounts.

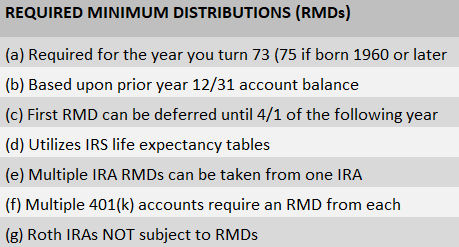

Required Minimum Distributions

A Traditional IRA, like 401 k and 403 b plans, require withdrawals at age 73. These are known as required minimum distributions or RMDs and they are included in your federal income taxes. If you direct all your retirement savings to pre-tax and tax-deferred accounts, you could be hit with a huge tax bill.

However, Roth IRAs are not subject to RMD rules. That means you can keep your retirement assets invested longer. Roth 401 k plans, on the other hand, are subject to RMD rules so exploring options to rollover those retirement assets to a Roth IRA may be beneficial.

SPECIAL NOTE: Due to the passage of SECURE 2.0 in late December 2022, item (a) in the chart below should read: Required for the year you turn 73.

Taxes On Social Security Income

Many people are surprised to find out they pay tax on Social Security income. If your taxable income is above a certain level, you can expect to pay income taxes on 85% of your Social Security benefits. It doesn’t matter when you file or what age you are.

Tax-Free Municipal Bonds

Munis offer interest payments that are tax-free which may benefit those in a higher tax bracket. However, you need to be careful because not all municipal bonds are alike. If you’re not careful, you may end up being hit with Alternative Minimum Tax or AMT.

In general, depending on your investment objective, risk tolerance, and tax bracket, tax-free munis have the potential to minimize taxes in retirement.

Health Savings Account

HSAs are designed to cover qualified medical expenses and not everyone can qualify. You need to be enrolled in a High Deductible Health Plan to be eligible.

Funds used to pay medical expenses are not included in taxable income. In other words, they’re tax-free.

Once you turn 65, you can withdraw funds from an HSA for any reason and only pay ordinary income tax. This would be the equivalent of taking a distribution from an IRA.

Unlike traditional IRAs, HSAs do not have required minimum distributions.

Qualified Charitable Distribution

As we discussed previously, Traditional IRA distributions are considered taxable income. However, at age 70 1/2 you become eligible for a QCD. This is where you use your IRA to make charitable contributions and reduce your tax bill. The amount you withdraw via a QCD is excluded from your taxable income.

Consider a scenario where you’re already making charitable contributions each year and you’re subject to RMDs. You can use part of your RMD as the Qualified Charitable Distribution. This will reduce the amount of taxable income you need to report to the IRS that would otherwise result from the RMD.

Net Unrealized Appreciation

Net Unrealized Appreciation or NUA is a retirement plan distribution strategy for those who hold highly appreciated company stock. Utilizing the NUA strategy can allow for the company stock within a 401(k) to be taxed at long-term capital gains rates as opposed to ordinary income rates.

Beware The Five-Year Waiting Rule For Roth IRAs:

The five-year waiting rule for Roth IRAs applies in two situations:

- In order to receive a qualified distribution of earnings (not principal) tax-free, the withdrawal must not be within 5 years of the date of the first contribution. These time periods are governed by the beginning of the tax year for which the contribution applies as opposed to the actual date.

- In order to receive a qualified distribution from a Roth IRA that was converted from an IRA without penalties applied to principal, the withdrawal must not be within 5 years of the date of the conversion.

How To Reduce Taxes In Retirement – Conclusion

Let’s face it, no one likes paying taxes. That’s especially the case during retirement. Utilizing tax diversification strategies and understanding basic tax laws could significantly reduce future tax bills.

Diversification isn’t just for investments. It is relevant for tax planning too. Rather than having all your retirement funds in one tax basket, diversify and allocate accordingly.

Have you considered how a Certified Financial Planner™ can help you?

As long as you are over 59 1/2 and have had your Roth IRA open for 5 years, all conversions from TIRA to the Roth IRA(with taxes paid on the conversion) are able to be withdrawn tax free including both the principle and earnings. IRS guidelines explain this well.

Thank you for contributing to the conversation Dan!

I’m3 years from reaching 65. I currently file MFS which appears it will affect my Medicare premium rate Plan B and D. I’d it common for switching to MFJ status.

Also, you mentioned that SS is taxed so here’s another eye opener. I’m assuming this figures into MAGI?

Great article!!

Javier

Thanks so much for the kind words. I’m glad you found the information helpful. Social Security is included in MAGI and factored in when determining Medicare premiums. As far as switching to MFJ, I’m not sure. I would be very careful because switching might help for one thing and hurt for another.