Whether you just started at MicroVu or you have been here for years, this guide is for you.

Some of you are engineers who want the details. Some of you have never invested a dollar in your life and just want to know what to do. Either way, this guide will help. We are going to cover how the 401(k) works, what your options are, and how to make sure your money is actually doing something for you, including when that bonus hits.

What Is a 401(k)?

A 401(k) is a retirement savings account tied to your job. Here is how it works in plain terms:

- You decide how much of each paycheck goes into it.

- That money gets invested and grows over time.

- You do not pay taxes on the gains until you retire, or in some cases, never. More on that below.

- You cannot touch the money without a penalty until age 59½, so it is meant to stay put.

The MicroVu 401(k) is held at Money Intelligence. That is where your account lives. If you have never logged in, that is your first step.

Never set up your 401(k)?

Contact HR in order to complete your enrollment, pick a contribution amount, and choose an investment. You do not need to have it all figured out to get started. Getting something in is more important than getting it perfect initially.

No Employer Match

As of March 2026, MicroVu does not match your contributions this is subject to change, but as now this means every dollar in your 401(k) you put it there yourself.

Some companies contribute extra money on top of what you save. MicroVu does not do that. And you should know that upfront.

But here is the part that trips people up: the 401(k) is still one of the best savings tools available to you. The tax benefits alone make it worth using, even without a match. We will get into that next.

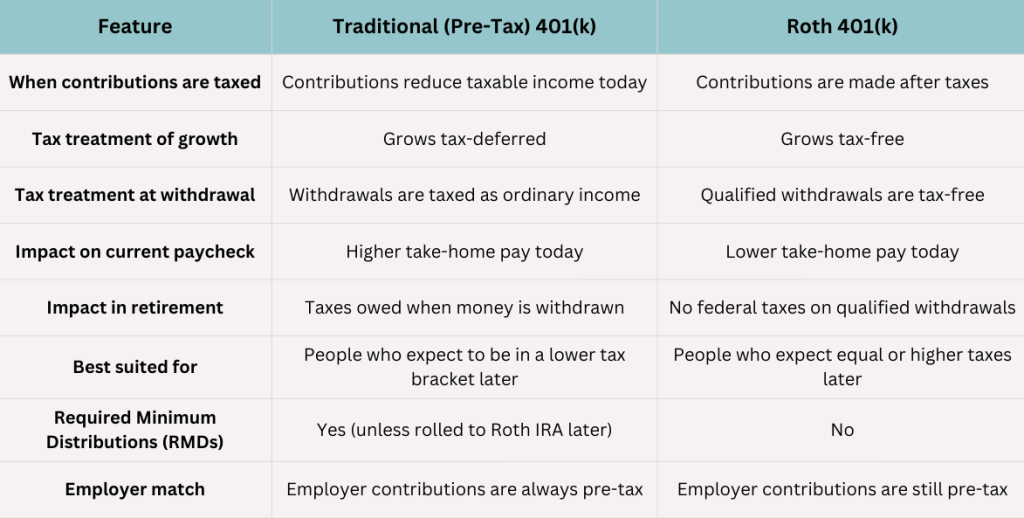

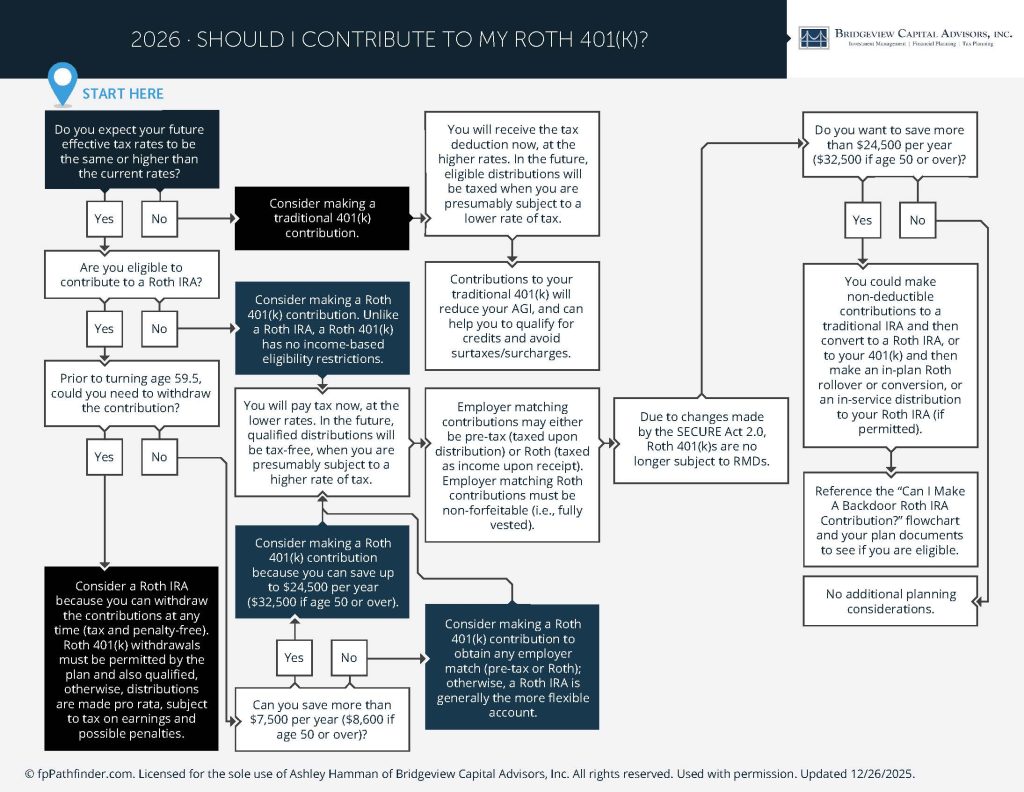

Roth vs. Pre-Tax

This is the most important decision inside your 401(k). Most people pick one without understanding the difference. Here is what you need to know.

Pre-Tax: Save on Taxes Now, Pay Later

When you contribute pre-tax, that money comes out of your paycheck before the government takes their share. Your taxable income goes down today, which means a slightly bigger take-home paycheck.

The catch: when you retire and start withdrawing the money, you pay income tax on every dollar you take out, including all the growth.

Roth: Pay Taxes Now, Never Pay Again

With Roth contributions, you pay taxes on the money before it goes into the account. No tax break today.

But when you retire and pull that money out? You pay zero tax. Not on the original contributions. Not on decades of growth. Nothing.

Which one should you pick?

For most MicroVu employees, especially those in their 20s and 30s, Roth is the better option. Here is why: if your income is lower now than it will be in 20 years, you are better off paying taxes now while your rate is low, and keeping all that future growth tax-free.

If you are older, higher-earning, the math might look different. The right answer depends on your situation. Working with a CERTIFIED FINANCIAL PLANNER® professional who can look at the full picture is highly recommended before making this choice.

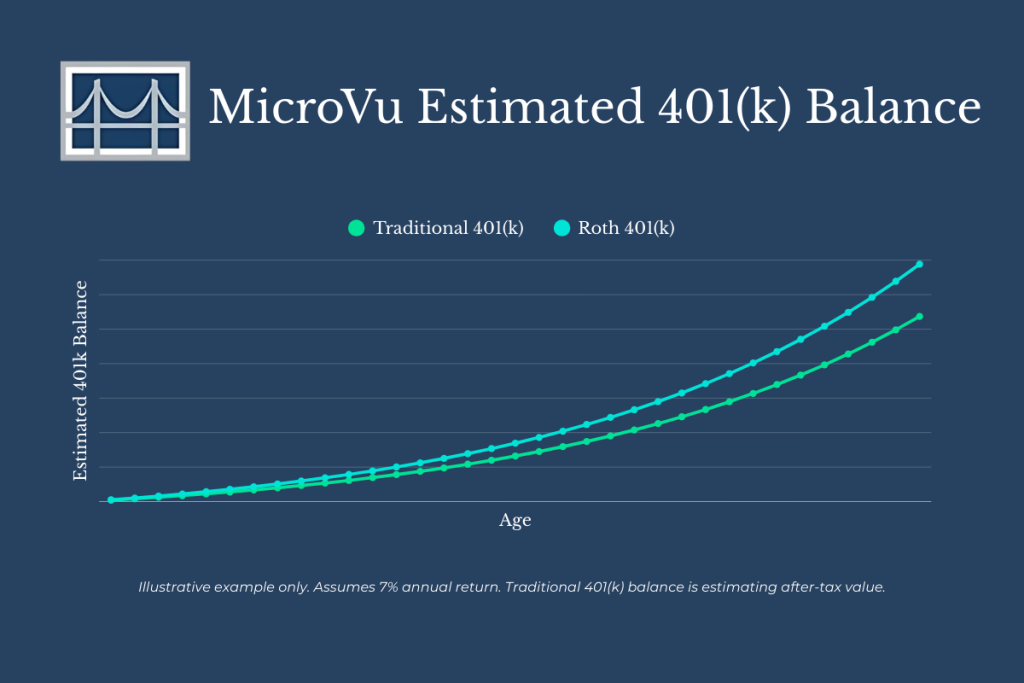

Why Roth Can Be a Big Deal

Say you are 28 years old and put $500 a month into the Roth 401(k). You do that for 35 years with an average 7% annual return. Your account grows to over $900,000. Because it is a Roth, you owe $0 in taxes when you retire. Every dollar is yours. If that had been pre-tax, you would owe income tax on the full amount when you withdraw it.

How Much Can You Put In Each Year?

The IRS sets limits on how much you can contribute. For 2026:

- Under age 50: up to $24,500 per year

- Age 50 or older: up to $32,500 per year (extra $8,500 catch-up)

- Ages 60 to 63: up to $35,750 per year under newer IRS rules

Most people are not close to the limit, and that is fine. The goal is not to max out immediately. The goal is to contribute consistently and increase it over time.

What to Do With Your Bonus

MicroVu gives out meaningful bonuses. That is genuinely great! But a bonus without a plan has a way of disappearing fast.

Here are some options worth considering when your bonus arrives:

- Increase your 401(k) contribution temporarily around bonus time so more goes in automatically.

- Build or top off an emergency fund. Three to six months of expenses in a regular savings account before investing more is a good benchmark.

- Pay off high-interest debt. A 20% credit card rate beats any investment return.

- Open a Roth IRA if you have not already. For 2026, you can contribute up to $7,500 per year ($8,600 if you are 50 or older). *Certain Income Limits Apply*

- Put the rest in a regular investment account, called a brokerage account, if your other buckets are covered.

The Common Mistake

The bonus hits the account and just sits in checking. No decision gets made, and three months later it is gone. If you get a $50,000 bonus every year and invested even just half of it, that adds up to a lot of money over a career! Give it a purpose before it shows up.

Your MicroVu 401(k) Investment Options

The plan has 25 investment options. That sounds like a lot. Here is how to think about them without getting lost.

Option 1: Target Date Funds

These are funds designed to do the work for you. You pick the one with the year closest to when you plan to retire. If you plan to retire around 2055, you pick the 2050 or 2060 fund.

The fund starts out invested aggressively (mostly stocks) when you are young, and automatically shifts to more conservative investments (more bonds) as you get closer to retirement.

Is it perfect? No. It does not know anything about your personal situation. But it is a simple starting point, especially if you do not want to manage it yourself.

Option 2: Build Your Own Mix

If you want more control, the plan has individual funds you can combine. Here is what the categories mean:

- U.S. Stocks — you are buying small pieces of American companies. Higher potential return, more short-term ups and downs.

- International Stocks — same idea, but companies outside the U.S.

- Bonds — loans to governments or companies. Lower returns than stocks, but more stable. Good for balancing out risk.

- Real Estate funds — invest in real estate without buying property.

- Balanced fund — a mix of stocks and bonds already blended together.

One number worth paying attention to in the table below: the expense ratio. That is the annual fee you pay just for owning the fund. It comes out automatically and most people never notice it, but it adds up.

Expense Ratios Add Up Fast

On a $200,000 account, a 1% expense ratio costs you $2,000 per year. A 0.05% expense ratio costs you $100 per year. Over 20 years, that gap in fees can cost you tens of thousands of dollars in lost growth. The Vanguard index funds in this plan are among the cheapest options available anywhere.

Full List of Investment Options

| Category | Fund Name | Ticker | 1-Year | 3-Year | 5-Year | Exp. Ratio |

| Target Date | T. Rowe Price Retirement 2010 | TRRAX | 11.75% | 10.88% | 4.98% | 0.49% |

| Target Date | T. Rowe Price Retirement 2020 | TRRBX | 12.53% | 11.70% | 5.61% | 0.51% |

| Target Date | T. Rowe Price Retirement 2030 | TRRCX | 14.38% | 13.77% | 6.78% | 0.55% |

| Target Date | T. Rowe Price Retirement 2040 | TRRDX | 17.46% | 16.68% | 8.44% | 0.59% |

| Target Date | T. Rowe Price Retirement 2050 | TRRMX | 18.81% | 17.89% | 9.22% | 0.62% |

| Target Date | T. Rowe Price Retirement 2060 | TRRLX | 18.97% | 17.97% | 9.24% | 0.64% |

| Balanced | Vanguard Balanced Index Adm | VBIAX | 13.58% | 15.24% | 7.75% | 0.07% |

| Intl Equity | DFA Emerging Markets Core Equity | DFCEX | 28.77% | 16.85% | 7.14% | 0.40% |

| Intl Equity | DFA Intl Core Equity | DFIEX | 36.15% | 18.49% | 10.38% | 0.23% |

| Intl Equity | Vanguard Emerging Mkts Index Adm | VEMAX | 24.75% | 14.77% | 4.62% | 0.13% |

| Intl Equity | Vanguard Total Intl Index Adm | VTIAX | 32.18% | 17.09% | 7.93% | 0.09% |

| Real Estate | PIMCO Real Estate Real Return A | PETAX | 5.19% | 7.21% | 5.84% | 5.89% |

| Real Estate | Vanguard Real Estate Index Adm | VGSLX | 3.19% | 6.58% | 4.64% | 0.13% |

| Bonds | Guggenheim Core/Core Plus Bond | GIBIX | 8.18% | 6.23% | 0.22% | 0.60% |

| Bonds | Guggenheim Macro Opportunities | GIOSX | 7.55% | 8.33% | 3.60% | 0.98% |

| Bonds | PIMCO Income A | PONAX | 10.60% | 8.14% | 3.48% | 0.94% |

| Bonds | PIMCO Intl Bond Fund USD Hdg A | PFOAX | 3.90% | 6.05% | 0.96% | 0.97% |

| Bonds | Templeton Global Bond Adv | TGBAX | 17.14% | 2.00% | -1.00% | 0.77% |

| Bonds | Vanguard Infl Prot Secs Adm | VAIPX | 6.87% | 4.15% | 1.03% | 0.10% |

| Bonds | Vanguard Total Bond Index Adm | VBTLX | 7.15% | 4.67% | -0.42% | 0.04% |

| Bonds | Vanguard Total Intl Bond Idx Adm | VTABX | 2.96% | 5.12% | -0.22% | 0.10% |

| U.S. Stocks | Dodge & Cox Stock Fund | DODGX | 13.65% | 15.20% | 13.32% | 0.51% |

| U.S. Stocks | Sphere 500 Fossil-Free Index F | SPFFX | 18.04% | 24.12% | N/A | 0.47% |

| U.S. Stocks | Vanguard Small-Cap Index Adm | VSMAX | 8.83% | 13.69% | 7.34% | 0.05% |

| U.S. Stocks | Vanguard Total Stock Index Adm | VTSAX | 17.12% | 22.23% | 13.06% | 0.04% |

How Much Risk Should You Take?

Every investment involves some level of risk. Stocks can go up fast and drop fast. Bonds are slower and more stable. The mix you choose determines how bumpy the ride is.

Two things to think about:

- How much does it bother you to watch your account drop? If a 20% dip would cause you to panic and move everything to cash, you probably have too much in stocks.

- How many years until you need the money? If retirement is 30 years away, short-term drops do not matter much. Your account will recover. If retirement is five years away, a big drop gives your account less time to recover

Young employees at MicroVu generally have time on their side. That means you can afford to take more risk and let the market work for you over the long haul. But that does not mean ignoring it entirely.

We offer a FREE risk assessment to help determine your mix of stocks & bonds. Click the link below to complete your assesment.

A simple rule of thumb

The further away retirement is, the more you can lean toward stocks. The closer you get, the more you shift toward bonds and stable options. A target date fund does this automatically. If you are building your own mix, revisit it often and consider getting a second option from a professional.

Frequently Asked Questions

Log into Money Intelligence. Make sure you are enrolled and contributing something. Even 5% of your paycheck is a start.

A general starting target is 10% to 15% of your income, but it really depends on the life you want to live and when you want to retire! Running a financial plan is a great way to see if you are track to meet your goals.

A raise is a good time to bump up your contribution percentage. Your paycheck is already going up, so routing some of that increase into your 401(k) before it hits your bank account is a great opportunity.

You can, but it usually costs you. Withdrawals before age 59½ are subject to a 10% penalty on top of regular income taxes. There are exceptions for hardship situations. Some plans also allow loans. Check with Money Intelligence for the specifics on the MicroVu plan.

Your account stays yours. You can leave it at Money Intelligence, roll it over to a new employer’s plan, or move it to an IRA.

Let’s Figure This Out Together

Reading this is a good start. But reading about your 401(k) and actually having a plan are two different things.

Here is what I do: I sit down with employees and go through their specific situation. What you make, what you have saved, what you want your life to look like when you retire. Then we figure out what to actually do, not what sounds good in theory.

A lot of people leave that first meeting feeling like a weight has been lifted. Not because everything is perfect, but because at least they know where they stand.

Ashley Hamman, CFP®, is a Vice President at Bridgeview Capital Advisors, Inc. She works with individuals and families on financial and tax planning and investment management, with a focus on helping people navigate real-life decisions with clarity and confidence as things change.