Integrated Financial Planning: Tax & Investments Working Together

I talk to people all the time who feel like they have things handled. They have a CPA they trust. A financial advisor managing their investments. Maybe a retirement plan they put together a few years ago. On paper, it looks like everything is covered.

And then I ask one question: do those people ever talk to each other?

Usually, the answer is no.

That’s the gap I want to talk about. Because you can do everything right, invest consistently, file your taxes on time… and still leave a significant amount of money on the table. Not because of bad decisions. Because of gaps between good ones.

Imagine going to your doctor for a complete physical. They run every test imaginable, blood pressure, lung function, reflexes, but only on the left side of your body. They hand you a clean bill of health and send you home.

You’d never accept that. Because your body is a system. What’s happening on one side directly affects the other. Something that looks perfectly fine in isolation might be a serious warning sign when you see the whole picture.

Your financial life works the same way.

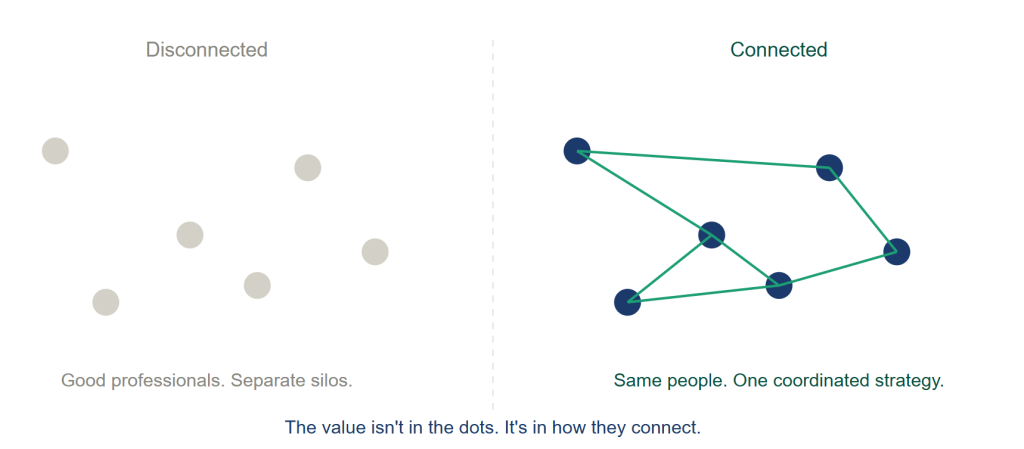

Tax planning, financial planning, and investment management share the same inputs: your income, your assets, your goals, your timeline. And they produce outputs that directly affect each other. Treating them as separate conversations isn’t just inefficient. It creates blind spots that can cost you real money over time.

That’s the hidden cost of fragmented financial advice. And I see it more often than you’d think.

The most expensive financial mistakes don’t happen in any single category. They happen in the gaps between them.

Where the gaps show up

Most people don’t experience this as one dramatic mistake. It shows up slowly, over time, in ways that rarely get traced back to the real cause.

A few Patterns I see regularly

Capital Gains

An investment manager rebalances a portfolio in December, triggering a capital gains event. The tax advisor learns about it in April. It’s too late to offset it.

Roth Conversions

A financial planner recommends a Roth conversion. No one checked that the client’s income was already elevated that year from a bonus. The conversion bumped them into the next bracket unnecessarily.

Retirement Planning

A client nearing retirement has accumulated almost everything in pre-tax accounts. Each advisor made sensible recommendations over the years. But no one was looking at the full picture and now there’s a significant and avoidable tax problem waiting in retirement.

Business Succession Planning

A business owner sells their company. The transaction is structured without coordinating with the investment manager or financial planner. Millions in proceeds land in the wrong accounts in the wrong year at the wrong tax rate.

None of these involve negligence or bad advice in isolation. They’re what happens when good professionals work on their part of the body without anyone ever seeing the whole patient. And most clients never realize the cost because there’s no statement that shows what could have been.

First, let’s talk about your CPA

I want to be clear about something before we go any further, because I don’t want this to sound like I’m criticizing CPAs. I’m not.

Your CPA plays a really important role. They make sure your return is filed correctly. They keep you compliant with tax law and catch mistakes. That’s valuable and it’s necessary.

But here’s the thing, a CPA’s job is to look backward. They take everything that happened last year and report it accurately to the IRS. By the time you’re sitting down with them in February or March, every financial decision that affected your taxes has already been made. The year is over and that window is closed.

Tax planning is different. It’s looking forward. It’s asking: given what we know about your income, your investments, your retirement accounts, and your goals right now. What should we be doing differently this year to reduce what you owe over your lifetime?

That’s not a CPA’s job. It’s not what they’re hired to do. And most of them don’t have the time or the full financial picture to do it even if they wanted to.

Think of it this way. Your CPA is there to make sure you’re filing correctly, like a compliance check. A financial planner doing proactive tax planning is trying to make sure you pay the least amount of tax possible over your entire life. Those are two completely different goals. And you need both.

Your CPA makes sure you file correctly. Tax planning makes sure you pay as little as possible over your lifetime. Those aren’t the same thing.

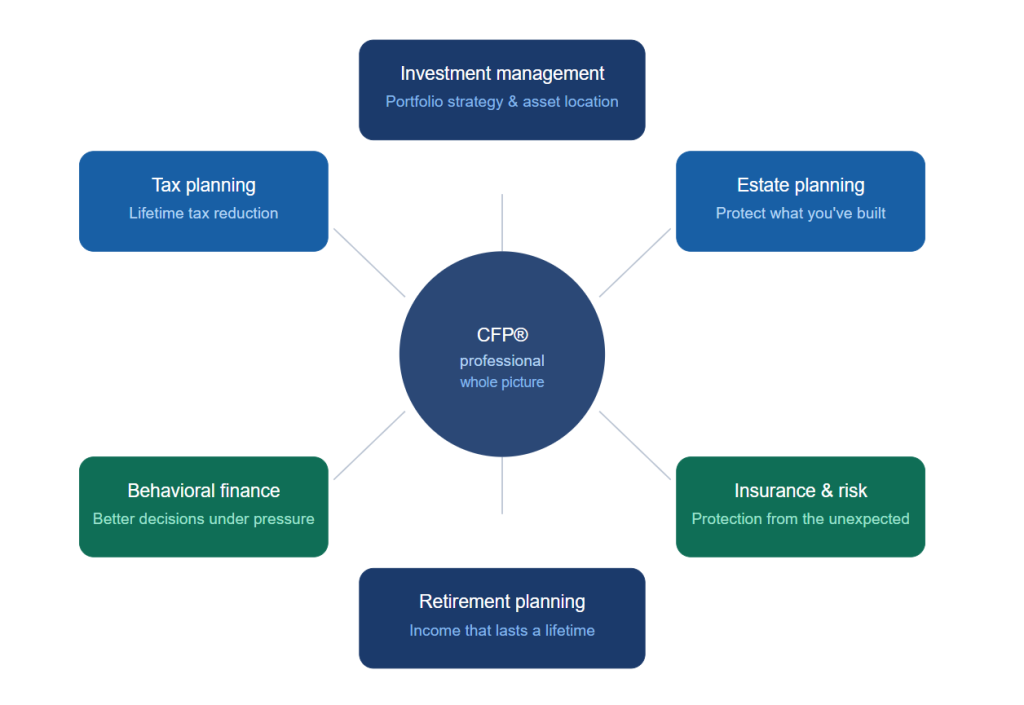

a CFP® professional is built to see the whole picture

This is where I think it’s worth explaining what a CERTIFIED FINANCIAL PLANNER® actually is because a lot of people don’t realize what goes into earning that designation.

It requires years of experience, a comprehensive education program, and passing one of the most difficult exams in financial services. And what makes it different from other designations is what it covers. A CFP® isn’t trained to be a specialist in just one area. They’re trained to understand how every part of someone’s financial life connects

Investment Management

Building a portfolio that fits your goals and timeline, putting the right investments in the right accounts, and understanding how your investments affect your taxes.

Retirement Planning

When you can retire, how much you need, how to draw down your accounts in the right order, and how to build income that lasts, not just a balance that looks good on paper.

Tax Planning

How to legally reduce what you owe, not just this year, but over your lifetime. Roth conversions, capital gains timing, bracket management, and how tax decisions ripple into everything else.

Estate Planning

What happens to your money and your family when you’re gone. Wills, trusts, beneficiary designations, and making sure your wishes actually get carried out the way you intend.

Insurance & Risk

Making sure the right protections are in place, life, disability, long-term care, so that one unexpected event doesn’t undo everything you’ve built.

Behavioral Finance

Understanding how emotions affect financial decisions and how to help people make better choices during the moments when it’s hardest to think clearly.

That last one, behavioral finance, tends to surprise people. But it might be the most important one. The best financial plan in the world doesn’t work if you panic and sell everything when the market drops, or keep putting off decisions because they feel complicated. A CFP® professional is trained to understand that side of money too.

The reason all of this matters here is simple. Integrated financial planning. Really connecting your taxes, your investments, and your financial plan requires someone who understands all of those pieces and how they affect each other. That’s exactly what the CFP® curriculum is built around.

What integrated financial planning actually means

Integrated financial planning means your tax strategy, your investment decisions, and your long-term financial plan aren’t three separate conversations. They’re one. Every decision is made with full awareness of how it affects the other two, before it’s made, not after.

That sounds simple, but in reality I’ve found it’s actually quite rare.

You need someone connecting the dots between these items. And those dots, the timing of a Roth conversion, the year a gain gets realized, the way charitable giving intersects with your tax bracket, are where the real planning happens.

When those dots aren’t connected, you end up with three specialists who each checked their half of the body and sent you home healthy. The problem nobody caught is still there. It just hasn’t shown up yet.

The Fragmented Approach

Your CPA files an accurate return. Your advisor rebalances on schedule. Your planner updates your retirement projections. Each professional does their job well, but none knows what the others are doing. The opportunities that live between them go unnoticed every year.

The Integrated Approach

Before any major move, strategy is coordinated across all three areas. Tax-loss harvesting is timed to offset gains. Roth conversions are calibrated to your bracket. Asset location is actively managed. Every decision is made in the context of the full picture, before the year closes.

Integrated Tax Planning in practice

I find that most people have never seen what proactive tax planning looks like in practice. So let me show you.

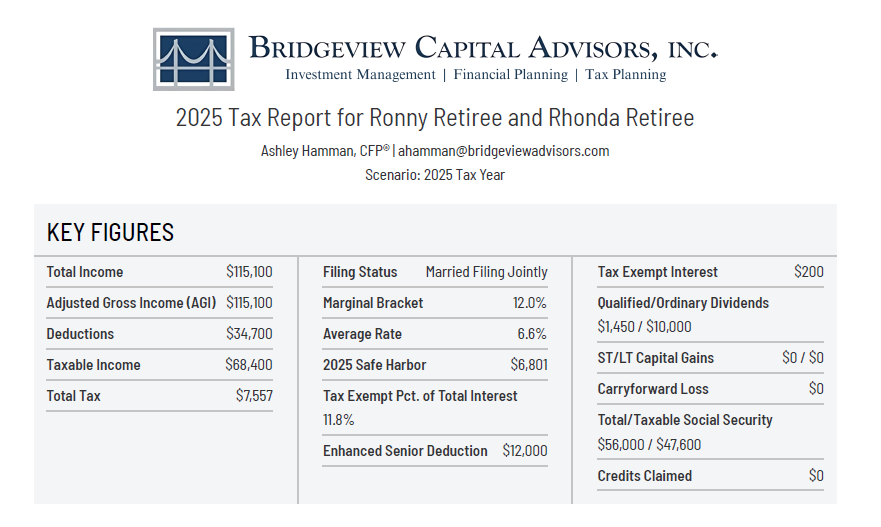

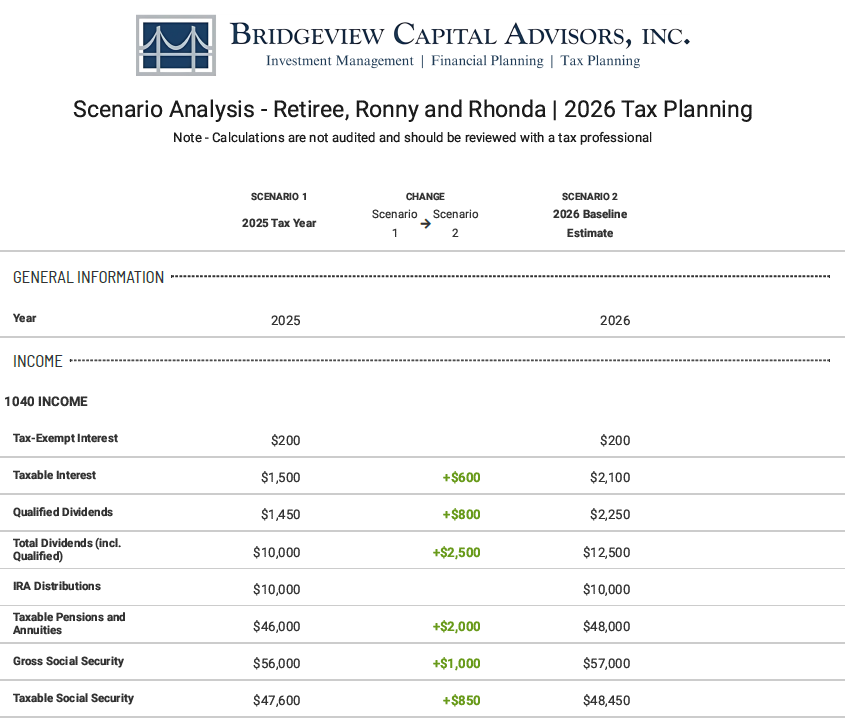

Here’s an example of what that annual review looks like for a sample client. Meet Ronny & Rhonda Retiree. They are a retired couple in El Dorado Hills age 75 and 71 who came into our office to learn more about integrated financial planning.

We started by reviewing Ronny & Rhonda’s most recent tax return and pulling out the numbers that matter most: total income, tax bracket, average rate, how much of Social Security is taxable, capital gains, and Medicare premium exposure. Think of it as a financial fingerprint. Before we can plan anything, we need to know exactly where they are.

This is the step most people have never had done for them. Instead of waiting until April to find out what you owe, we estimated Ronny & Rhonda’s current year tax bill.

Knowing this well before the end of the year means there’s still time to do something about it.

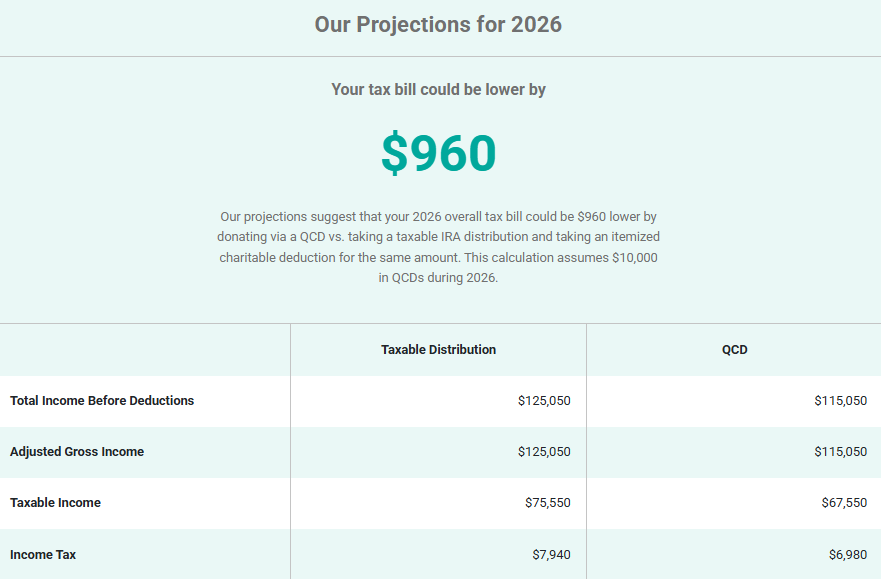

We showed them exactly what their total tax will be for 2026. In this case it was $7,940.

After withholdings, they will get a refund of ~$2,060.

Now here is where we can nerd out. Based on the 2026 estimate Ronny & Rhonda’s tax return, we can analyze different strategizes to lower total tax paid over their lifetime. For these clients, we noticed they were already donating $10,000 cash to charity each year. We instead recommended they stopped writing these checks from their bank accounts and instead wrote them out of their IRA account, which is known as a Qualified Charitable Distribution (QCD).

We then created another scenario of how this strategy would compare to our 2026 estimate.

The Result: Ronny & Rhonda’s tax bill dropped by almost $1000.

Every year, we run each client through a full tax review. It gives us a clear picture of where you stand today, and what moves make sense before the year closes.

Integrated financial planning

When tax planning, financial planning, and investment management are actually coordinated, the decisions look different.

Your Roth conversion strategy is built around your real tax bracket. The retirement plan maps out which accounts to draw from first and in what order, so you pay less tax over your lifetime. Charitable giving is structured around your income that year, not just your generosity. And when something big happens: a new job, an inheritance, a business sale, the whole plan gets looked at together. Not three separate phone calls that never quite connect.

That’s what integrated financial planning actually means. Someone looking at the whole body and making decisions with the full picture in view.

It’s how we work with every client at Bridgeview Capital Advisors, Inc. As a fee-only, fiduciary firm in El Dorado Hills, CA, we bring tax planning, financial planning, and investment management together into one coordinated strategy. Our advice is built around your complete picture.

What You should consider with integrated Financial Planning

If any of those felt unfamiliar, that’s okay. It doesn’t mean you’ve done anything wrong. It usually just means nobody has looked at the full picture yet. And there’s almost always something worth looking at if you start before the decisions are already locked in.

Your finances are a system too. And systems need someone looking at all of it, not just their piece of it.

That’s what we’re here for.

Frequently asked questions

A CERTIFIED FINANCIAL PLANNER® professional has passed a rigorous exam and met experience requirements covering every major area of personal finance: tax planning, estate planning, retirement, investments, insurance, and behavioral finance. Unlike the title “financial advisor,” the CFP® designation means someone has been trained to understand how all the pieces of your financial life connect and affect each other and they are held to a fiduciary capacity, meaning their advice is in your best interest.

A CPA’s job is to make sure your tax return is filed correctly and that you’re compliant with tax law. That’s important and you need it! But it’s backward-looking. By the time you’re filing, all the decisions that affected your taxes have already been made. A financial planner doing proactive tax planning looks forward, figuring out what your taxes will look like next year and making strategic moves before the year closes to reduce what you owe over your lifetime. Both matter. They just do different things.

It means your tax planning, investment management, and financial planning aren’t three separate conversations. They’re one coordinated strategy. Every decision is made knowing how it affects your taxes, your investments, and your long-term goals at the same time. At Bridgeview Capital Advisors, Inc. , that coordination is built into how we work with every client.

You can, and it helps. But in practice it tends to be reactive. This mean information often gets shared after decisions are already made. Real integration means strategy is built together before anyone moves, with everyone looking at the same full picture from the start.

A fee-only advisor gets paid only by you. They are not through commissions or product sales. That matters because it removes the conflicts of interest that can push advice in the wrong direction. When we make a recommendation, it’s because it’s the right move for your situation. Not because it earns us anything.

Our #1 requirement to become a client is that you have to be nice! We love working with individuals, families, and business owners in El Dorado Hills and the greater Sacramento area, including Folsom, Granite Bay, and Roseville, who want a fee-only, fiduciary bringing their tax planning, financial planning, and investment management together into one strategy that actually makes sense as a whole.

Ashley Hamman, CFP®, is a Vice President at Bridgeview Capital Advisors, Inc. She works with individuals and families on financial and tax planning and investment management, with a focus on helping people navigate real-life decisions with clarity and confidence as things change.