Estate Tax Planning: The Mistake That Cost Prince Millions (Photo Credit NPG)

When Prince died suddenly in 2016, the world lost a musical icon. But behind the scenes, something else happened, something far more ordinary, and far more dangerous for anyone with wealth. It’s actually one of the most common mistakes in estate tax planning.

Prince died without a will. Without a trust. And without a plan.

And the financial consequences were massive.

Estate problems don’t start when you’re wealthy.

They start when you wait.

Let’s break it down in plain English.

The mistakes Most People Make

Most people believe some version of this:

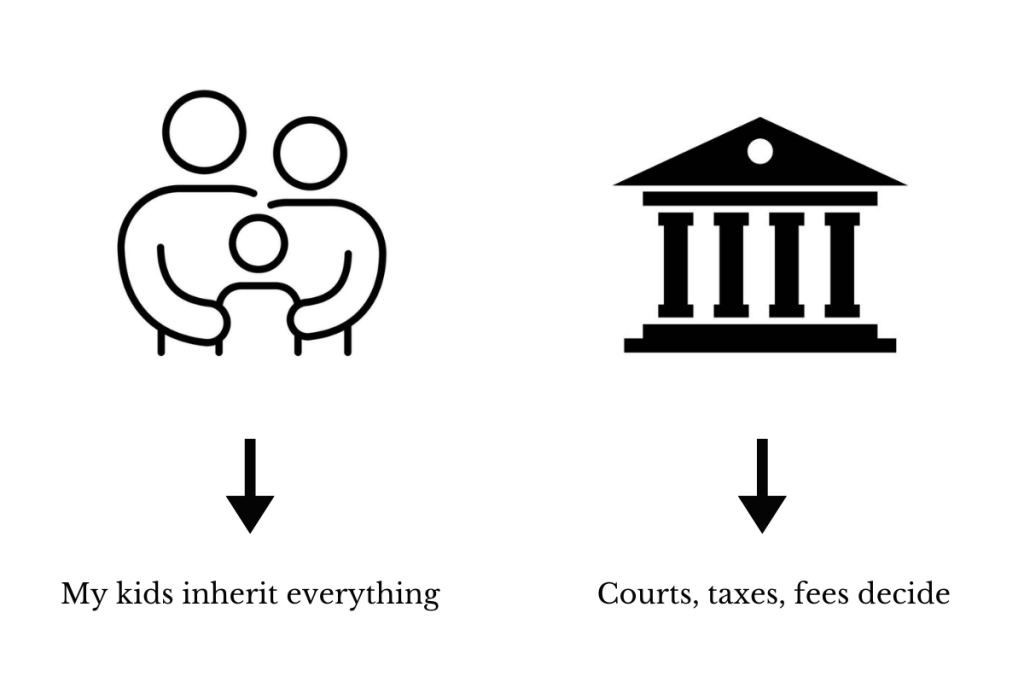

“If something happens to me, my money will go to my kids.”

But Prince’s story shows exactly why that assumption can be wrong and costly.

What Prince’s Story Actually Teaches Us

Prince didn’t lack money.

He lacked instructions.

Because there was no estate plan:

- The courts stepped in

- The government took first priority

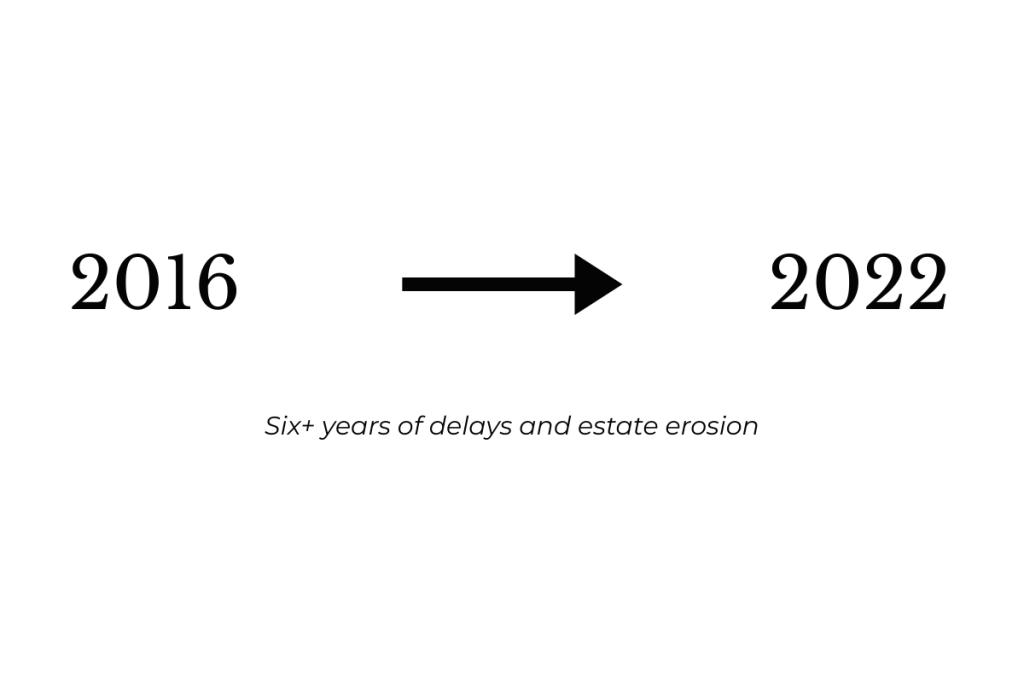

- Lawyers, accountants, and administrators billed the estate for years

- Decisions dragged on for more than six years

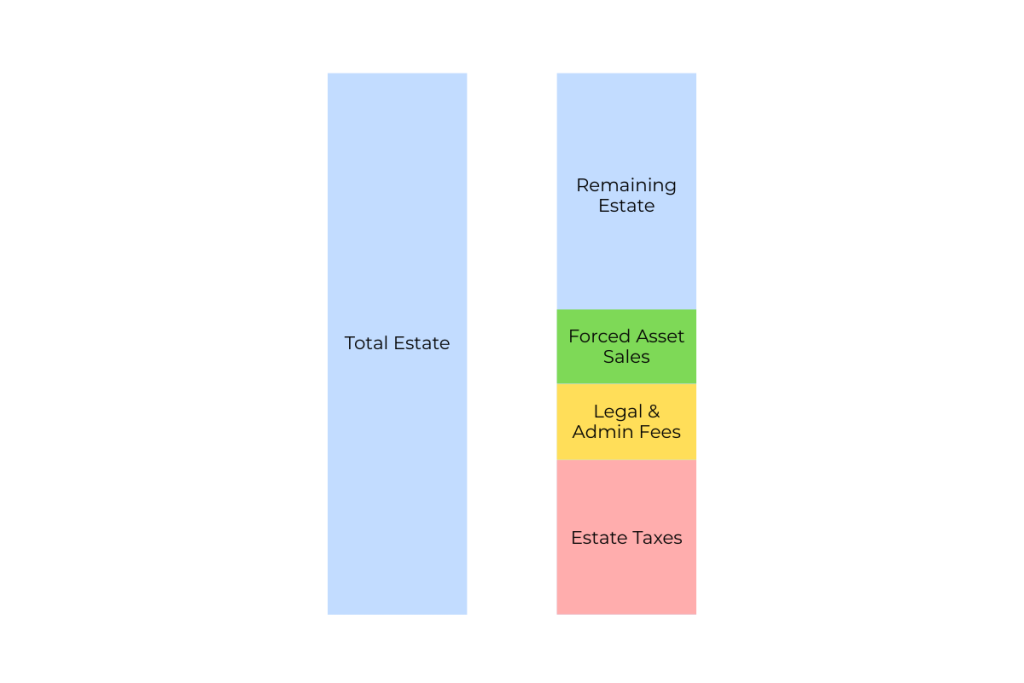

By the time things were resolved:

- Tens of millions were paid in estate taxes

- Millions more were lost to legal, administrative, and penalty costs

- A significant portion of Prince’s legacy ended up outside the family, sold to corporations just to untangle the mess

Less than half of the original estate value remained for heirs and interests connected to the family.

Why Prince’s Story Matters to Californians

You don’t need a $150M estate to face a similar fate. For high-net-worth professionals in El Dorado Hills, California, the same forces are at work:

High property values, homes often $2–5M or more

Appreciating investments, portfolios, retirement accounts, and business equity grow over time

Legal and probate fees can cost 2–5% of the estate.

The mechanics are the same as Prince’s estate: growth + taxes + friction = wealth lost to things outside your family.

A Realistic Example of Poor Estate Tax Planning

Let’s take a high-net-worth individual living in El Dorado Hills, CA:

- Estate value: $20 million (home, investments, business equity, retirement accounts)

- Federal estate tax exemption: $15 million

- Federal estate tax rate: 40% on taxable portion

- Professional/legal/probate fees: ~$1 million

- Children: 3

If this person were to pass away today, here is how this estate could look like.

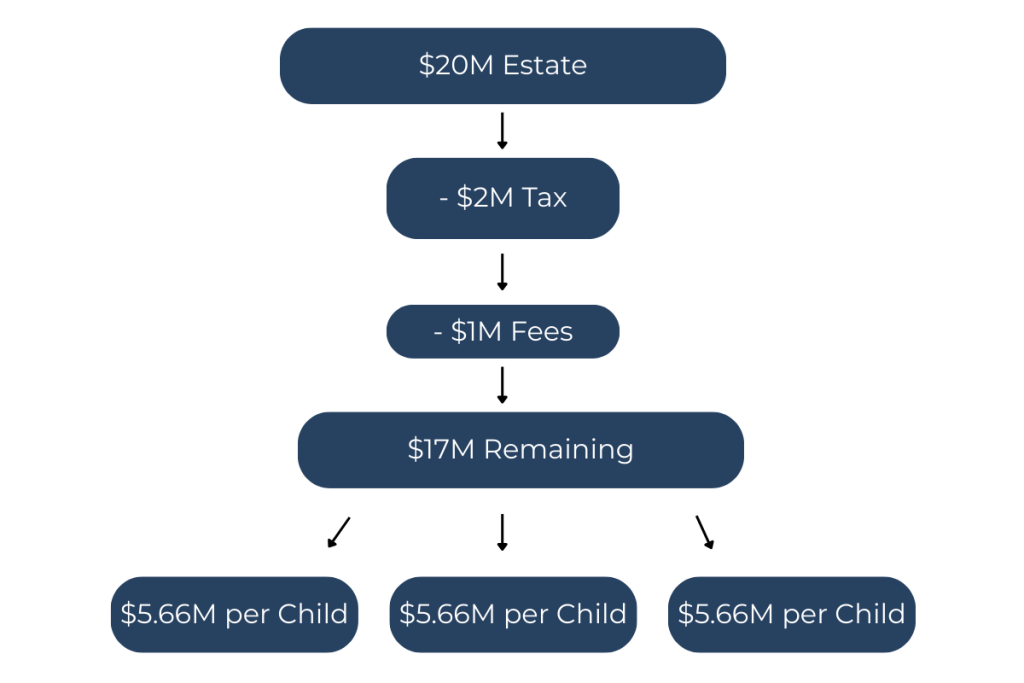

Step 1: Taxable estate

$20M – ($15M estate exemption) = $5M taxable estate

Step 2: Federal estate tax

$5M taxable estate × 40% = $2M Owed in Estate Taxes

Step 3: Fees

~$1M for legal, accounting, probate

Step 4: Net estate for heirs

$20M Total Estate − $2M Taxes − $1M Lega/Admin Fees = $17M Remaining

Divided among 3 children → $5.67M each

That’s $1M per child lost before anyone touches the inheritance.

That might not sound like a lot, but remember that is $3M total lost due to lack of planning and something that can easily be avoided.

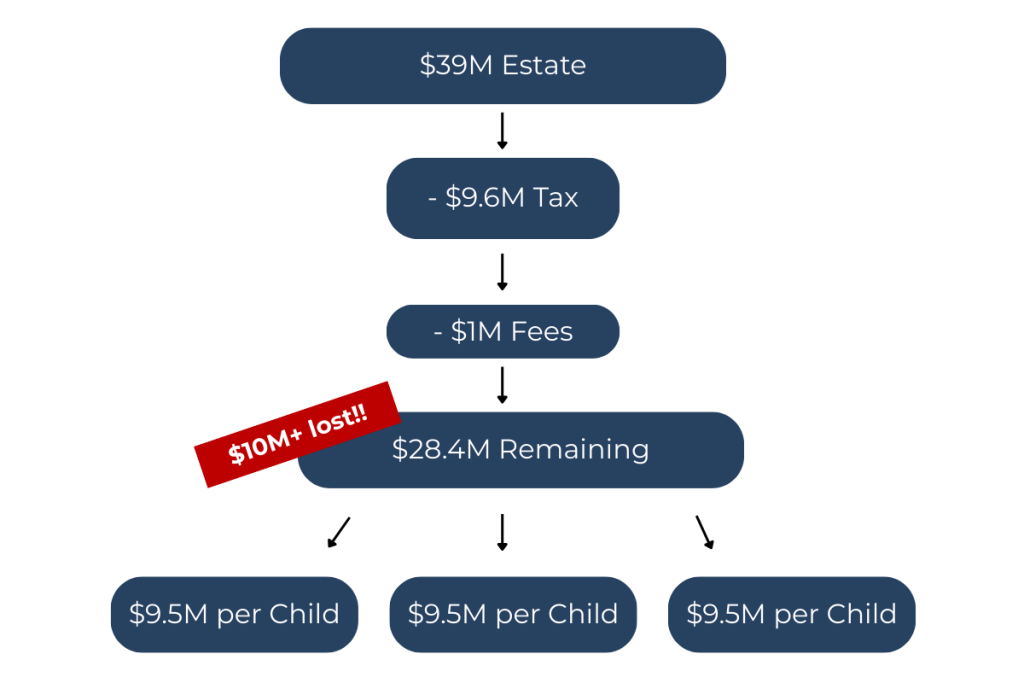

Also, this is assuming they pass TODAY. What if it’s not for another 10+ years?

Step 5: Add growth (the hidden trap)

High-net-worth estates often grow quickly:

- $20M today → 7% annual growth → ~$39M in 10 years

- Taxable estate = $39M Estate – ($15M estate exemption) = $24M taxable estate

- $24M taxable estate × 40% = $9.6M Owed in Estate Taxes

- ~$1M for legal, accounting, probate

Net estate ≈ $28.4M → per child ≈ $9.5M

Without planning, almost $10M could be lost.

Why Estate Tax Planning Matters More Than the Exemption

Even with today’s $15M federal exemption, wealthy California families can:

- Lose millions if assets grow inside the estate

- Pay unnecessary fees and delays

- Have their kids inherit far less than expected

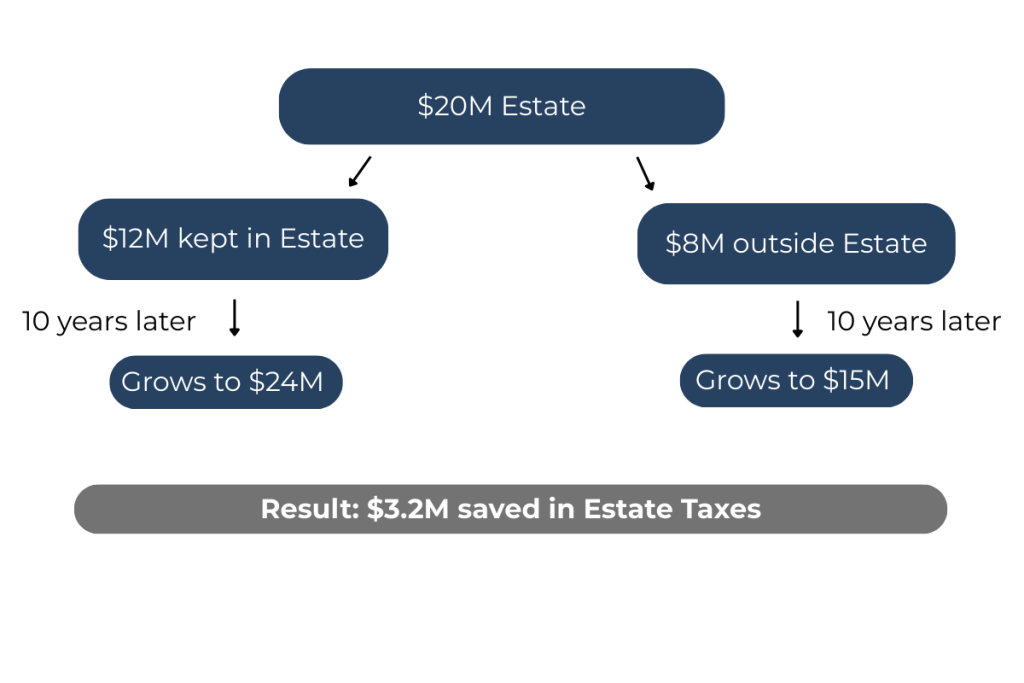

It’s not what you have today that matters. It’s what you have when you die, and how much of that growth the government can claim.

How Families Can Protect Their Estate tax planning

Just like Prince’s heirs could have benefited from proper planning, EDH families can:

- Move growth outside the estate

- Use exemptions efficiently

- Minimize probate and fees

- Update plans regularly. Growth, lifestyle changes, and law updates impact your estate

The estate planning mistake Most People Don’t Realize They Can Control

Here’s the good news.

Estate planning isn’t just about deciding who gets what.

It’s about deciding:

- Where future growth lives

- How much stays exposed to estate taxes

- How much compounds outside your estate altogether

You can do work now so tomorrow’s growth isn’t taxed later.

That means:

- Freezing today’s value

- Letting future appreciation grow separately

- Reducing what the government ever gets a claim on

- Preserving more wealth for your family

This is where timing matters more than complexity.

why Waiting Is the biggest estate tax planning mistake

The biggest mistake successful professionals make isn’t bad investing.

It’s waiting until:

- Their net worth already crossed the line

- Options are limited

- Time is no longer on their side

Planning earlier means:

- Smaller, simpler moves

- More flexibility

- Less disruption

- Significantly better outcomes

Once wealth grows, moving it becomes harder.

Once time runs out, it becomes impossible.

This is the Line That Matters Most

Because when life ends unexpectedly, the government already has a plan for your money.

And it may not match yours.

Because when life ends unexpectedly, the government already has a plan for your money. And it may not match yours.

Estate planning is how you make sure success actually reaches the people you worked your whole life for.

Why We’re Sharing This

At Brideview Capital Advisors Inc., we work with affluent professionals to help you:

The Question to Ask Yourself Today

If your net worth doubles over the next 10–15 years, and for many successful professionals, it will. Ask yourself:

- How much of that growth is exposed to estate taxes?

- How much could be growing outside your estate?

- What happens if you don’t get a second chance to fix it?

If you don’t know the answers, that’s your signal.

Take the Next Step

Reach out to Brideview Capital Advisors, Inc. today to begin your estate planning conversation, before time (& Uncle Sam) makes the decisions for you.

Frequently Asked Questions

Because he had no will or trust. Without instructions, courts and tax authorities controlled the process.

Yes. Depending on timing, laws, and state taxes, 30–45% of an estate can be lost without planning.

No. Anyone with growing assets, real estate, or a business can face these issues sooner than expected.

Yes. Planning early allows future growth to occur outside the taxable estate, which can dramatically improve outcomes

Before you think you “need” to. The earlier you plan, the more control you keep.