What are Trump Accounts?

Trump Accounts are a new type of investment account for children, scheduled to launch July 5, 2026. The program helps families save and invest for a child’s future.

Days Until Trump Accounts Launch

Key Facts

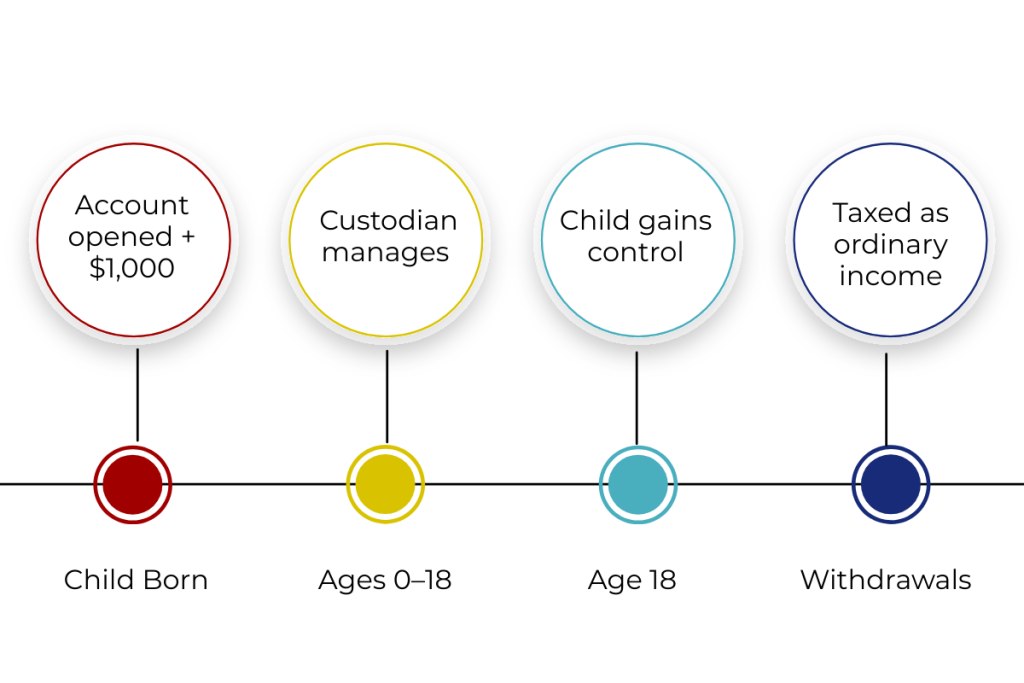

- The account is in the child’s name.

- Parents or legal guardians manage the account until age 18.

- Eligible children (born 2025–2028) may receive a $1,000 government contribution.

- Families, friends, or employers can contribute up to $5,000 per year per child.

- The money invests in a mix of U.S. companies through low-cost index funds.

- At age 18, the child takes full control of the account.

- Funds may be used for education, a first home, or starting a business.

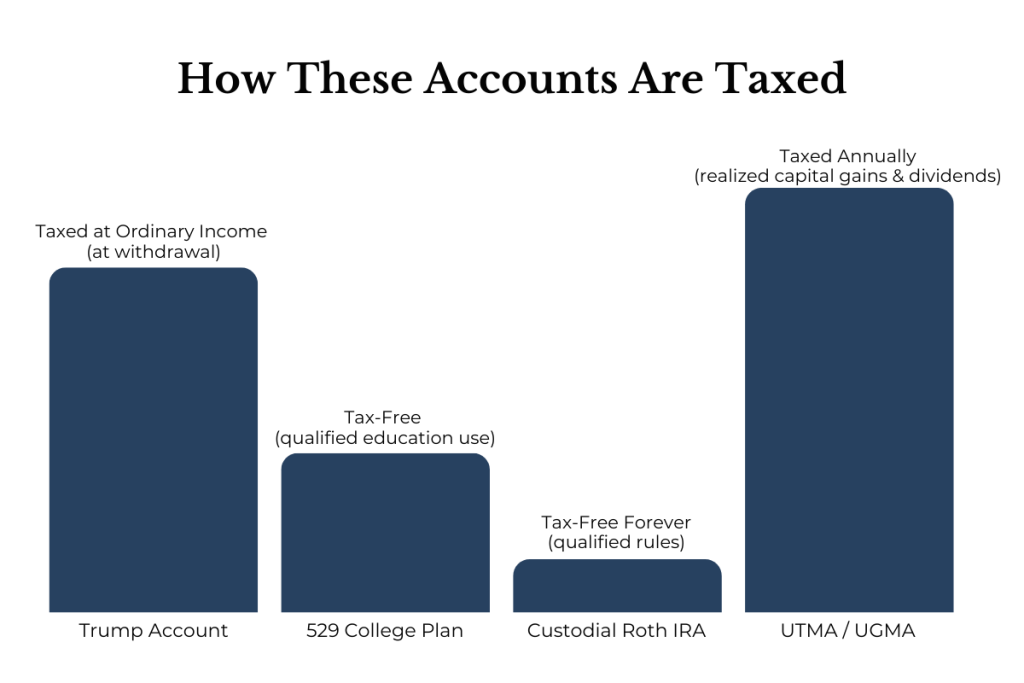

This is important: The IRS taxes withdrawals at your normal income tax rate. This works similar to a 401(k) or traditional IRA. With accounts like this, it’s important to remember the government will tax the money later.

What we Still Don’t Know with Trump Accounts

Trump Accounts launch in less than four months, but lawmakers still have not clearly explained several important details. Before families rely on these accounts as a long-term plan, we need clearer answers on how the rules will actually work.

Here is one of the biggest questions:

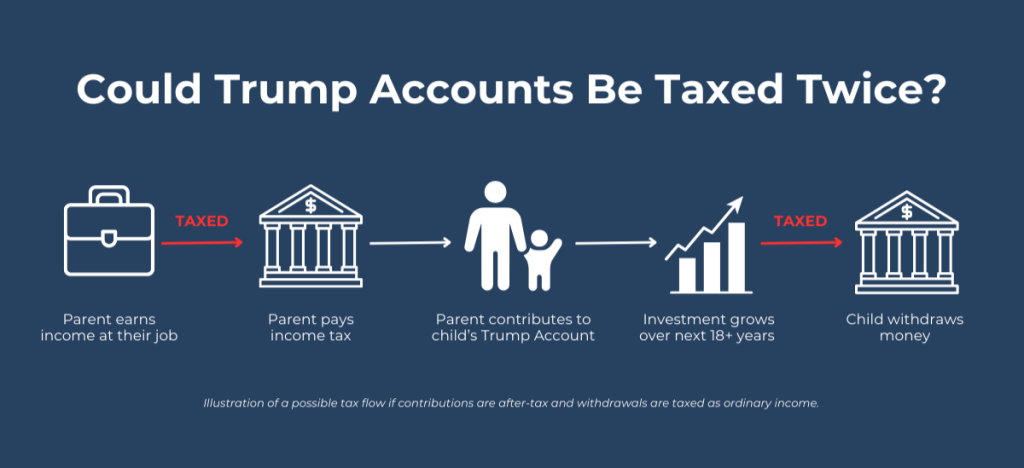

Will parents get a tax deduction for contributions?

Right now it appears parents contribute with after-tax money, meaning you do not get a tax break when you put the money in.

If parents do not get a deduction, they contribute after-tax dollars. Then years later, the IRS may tax the money again when the child withdraws it. This could mean families pay tax twice — once when the money is earned and again when it is taken out.

There is also the possibility that parents may need to keep detailed records of how much they contribute over the years. This would help determine what portion of a future withdrawal is taxable.

These are not small details and will directly affect how valuable these accounts will be for families.

Take the $1,000

If your child qualifies, open the account and capture the $1,000.

That’s an instant gain.

But after that, you evaluate where additional dollars should go.

Why? Because taxes have a big impact on long-term growth.

How to Open a Trump Account

1. Complete IRS Form 4547 to elect a Trump Account.

2. A participating financial institution receives the funds and activates the account. You’ll need:

a. Dates of birth

b. Contact information

c. Social Security numbers for you and your child

3. You can submit up to two children per form (additional children require another form).

Other Accounts to Consider Alongside Trump Accounts

529 plans

A 529 Plan is an investment account that helps families save for education costs and offers tax benefits.

Key Facts

- The account is opened for the benefit of a child (beneficiary).

- A parent, grandparent, or other adult owns and controls the account.

- Contributions are made with after-tax dollars.

- Some states offer a state income tax deduction for contributions.

- Funds grow tax-deferred.

- Withdrawals are tax-free when used for qualified education expenses.

- Can be used for college, trade schools, and up to $10,000 per year for K–12 tuition.

- Limited ability to change the beneficiary to another family member.

- Recent rules allow limited rollover to a Roth IRA (subject to restrictions).

This is important: Growth is tax-free if used for qualified education expenses OR if you roll it over to a Roth IRA

Custodial Roth IRA

A Custodial Roth IRA is a retirement account opened for a minor who has earned income. Earned income means money the child works for, like a job, babysitting, or lawn care.

Key Facts

- The account is opened in the child’s name.

- A parent or guardian manages the account until age 18 or 21 (depending on state).

- The child must have earned income to contribute.

- Contributions are limited to the child’s earned income (up to annual IRS limits).

- Contributions are made with after-tax dollars.

- Investments grow tax-free.

- Funds can be invested in stocks, bonds, mutual funds, ETFs, etc.

- Contributions (not earnings) can be withdrawn anytime without penalty.

- Earnings can be withdrawn tax-free after age 59½ (if rules are met).

- Funds can also be used for a first home purchase (up to $10,000) or certain education expenses without penalty.

This is important: The IRS will not tax the money again if withdrawal rules are followed.

Custodial Accounts (UTMA/UGMA)

A Custodial Account (UTMA/UGMA) is a taxable investment account opened for a minor, allowing assets to be held in the child’s name.

Key Facts

- The account is opened in the child’s name.

- A parent or guardian manages the account until the age of majority (18 or 21, depending on state).

- Anyone can contribute to the account.

- There are no annual contribution limits (though gift tax rules apply).

- Funds can be invested in stocks, bonds, mutual funds, ETFs, etc.

- The custodian can use the money for any expense that benefits the child.

- At the age of majority, the child gains full and irreversible control.

- Assets count as the child’s asset for financial aid calculations.

This is important: Investment growth is taxable each year under “kiddie tax” rules.

Account Comparison Chart

| Feature | Trump Account | 529 College Savings Plan | Custodial Roth IRA | Custodial Brokerage (UTMA/UGMA) |

|---|---|---|---|---|

| Best For | Supplemental Savings | Education | Long-Term; Retirement | Flexible Gifting |

| Who Owns the Account | Child; Custodian Controls Until Age 18 | Individual Who Opens and Controls the Account (typically parent or grandparent) | Child; Custodian Controls Until Age 18 | Child; Custodian Controls Until Age of Majority (varies by state) |

| Annual Contribution Limit | $5,000 | Annual IRS Limit 2026 – $19,000 ($38,000 if Married filing jointly) without potentially incurring a gift tax Can also superfund (5 year’s worth of exclusions at once) | Annual IRS Limit 2026 – $7,500 | Annual IRS Limit 2026 – $19,000 ($38,000 if Married filing jointly) without potentially incurring a gift tax |

| Investment Management | Index Funds | Age-Based or Static Asset Allocations | Very Flexible – Stocks, Bonds, ETFs, etc. | Very Flexible – Stocks, Bonds, ETFs, etc. |

| Tax on Growth | Ordinary Income at Withdrawal | Tax-Free (Qualified Use) | Tax-Free (Qualified Use) | Tax Annually on Realized Capital Gains & Dividends |

| Use Restrictions | Education, First Time Home Purchase, or Starting Business | Education-Focused; May also be eligible for rollover to Roth IRA | Tax-free after age 59½; You can withdraw contributions at any time; IRS allows additional exceptions for early withdrawals | None |

| Initial Government Contribution | Yes ($1,000 eligible children) | No | No | No |

| Tax Efficiency | Moderate | High | Very High | Low |

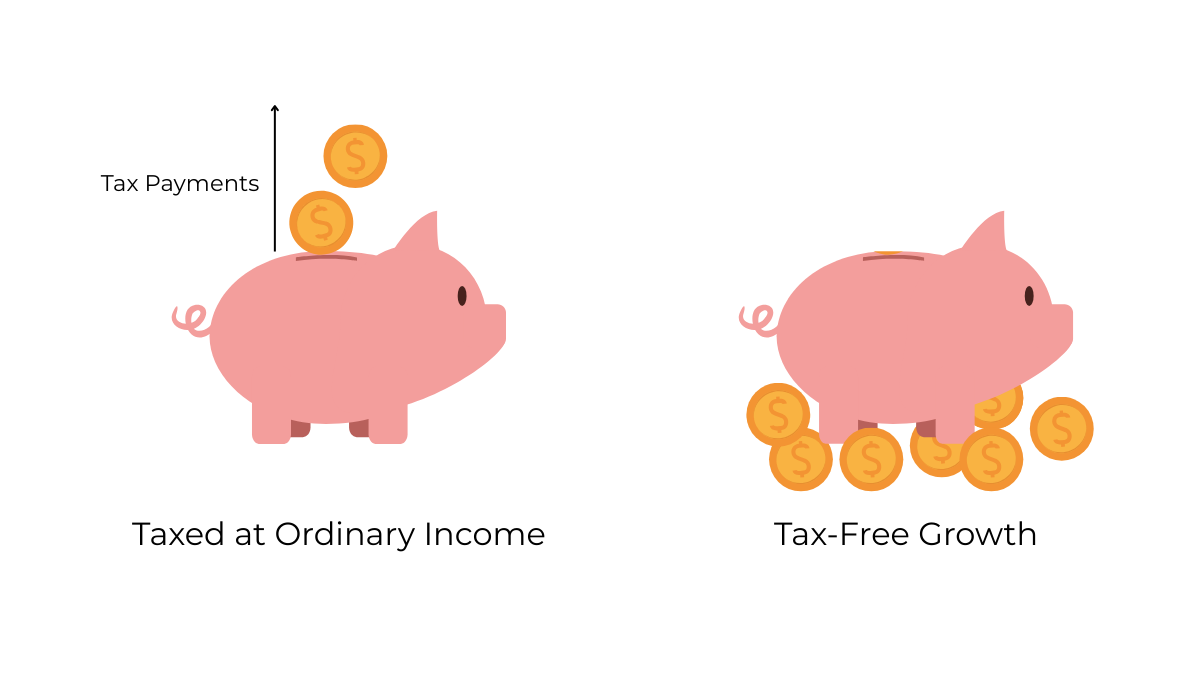

The Bigger Question for Trump Accounts

If you’re saving for your child for the next 18 years…

Where should most of that growth happen?

In an account taxed at ordinary income?

Or in one designed to avoid taxes completely?

That decision matters far more than the initial $1,000.

Work With Bridgeview Capital Advisors, Inc.

At Bridgeview Capital Advisors Inc., we help families:

- Prioritize tax-efficient custodial strategies

- Coordinate education and retirement planning

- Review new government programs carefully

- Build long-term plans that grow over time

New accounts create opportunity.

But disciplined structure creates wealth.

If you’re wondering how a Trump Account fits into your broader plan, schedule a conversation with Bridgeview Capital Advisors, Inc. today.

Let’s make sure every dollar has a purpose.

Frequently Asked Questions

A Trump Account is a government-supported investment account for children expected to launch in July 2026. Eligible children receive a $1,000 government contribution, and a parent or guardian manages the account until the child turns 18.

Any U.S. citizen child under age 18 with a Social Security number can have a Trump Account opened by a parent or legal guardian.

However, the $1,000 government contribution only applies to children born between 2025 and 2028. Children born earlier can still open an account and receive contributions from family members or employers, but they will not receive the federal deposit.

Parents, family members, and employers can contribute up to $5,000 per year per child. The account invests contributions in a diversified portfolio of U.S. companies, typically through low-cost index funds.

Money from a Trump Account can be used for:

– Education expenses

– Buying a first home

– Starting a business

Withdrawals are taxed at the child’s ordinary income tax rate.

Trump Accounts provide a $1,000 government contribution, but withdrawals are taxed as ordinary income.

By comparison:

– 529 Plans offer tax-free growth and withdrawals for qualified education expenses.

– Custodial Roth IRAs offer tax-free growth and withdrawals, but require the child to have earned income.

Because of the tax treatment, Trump Accounts are generally less tax-efficient than 529 plans or Roth IRAs for long-term savings.

Ashley Hamman, CFP®, is a Vice President at Bridgeview Capital Advisors, Inc. She works with individuals and families on financial and tax planning and investment management, with a focus on helping people navigate real-life decisions with clarity and confidence as things change.