If you work at Sanofi, you may be participating in the company’s 401(k) plan and wondering whether you are on track.

Most people want to save for retirement. They want to make good decisions. The challenge is that employer retirement plans, including the Sanofi 401(k), are full of unfamiliar terms, plan-specific rules, and choices that are rarely explained in plain English.

What Is the Sanofi 401(k) Plan?

The Sanofi 401(k) plan is a workplace retirement plan that allows eligible employees to save for retirement through payroll contributions.

Employees can generally contribute on a pre-tax basis, a Roth basis, or a combination of both. Contributions are invested among a variety of options selected by the plan, and the account grows over time based on contributions and investment performance.

Eligibility and Participation

Most employees become eligible to participate in the Sanofi 401(k) plan immediately.

Once enrolled, contributions are deducted automatically from each paycheck. Employees can usually adjust how much they contribute and how the money is invested through the plan’s online portal.

If You’ve Left Sanofi: 401(k) Options for Former Employees

If You’ve Left Sanofi: 401(k) Options for Former Employees

Even after leaving Sanofi, your 401(k) account stays in your name at T. Rowe Price. You have a few options for what to do next:

Keep your money in the Sanofi 401(k). This is the simplest choice. Your account stays invested in the plan, but you’ll still be subject to the plan’s rules and requirements.

Roll it over to an IRA or a new employer plan. Moving your 401(k) to an IRA or another workplace plan can give you more flexibility or consolidate accounts. With an IRA, you can choose from a wider range of investments and are no longer limited by the Sanofi plan rules.

Take a distribution. This is usually less favorable before retirement because of taxes and penalties. It may make sense in certain situations.

Each option has different tax rules and timing considerations. Think about how a rollover or withdrawal fits your broader financial picture, especially if you are retiring, or your income has changed.

Sanofi 401(k) Plan Login & Contacts

The Sanofi U.S. Group Savings Plan is administered by T. Rowe Price. Employees can manage their 401(k) account, review balances, update investments, change contribution amounts, and access plan tools through T. Rowe Price’s online portal.

|

Plan Name |

Sanofi U.S. Group Savings Plan |

|

Website |

|

|

Phone |

(800) 922-9945, Monday – Friday, 4:00 a.m. to 7:00 p.m. PST. Automated voice response system available 24/7 |

|

Fax |

(410) 581-5176 |

|

Mailing Address |

P.O. Box 17215 Baltimore, MD 21297 |

If you need help with enrollment, contribution changes, investment options, or account access issues, T. Rowe Price is the primary point of contact for the plan.

Employer Match and Vesting

Sanofi offers a remarkably generous employer match.

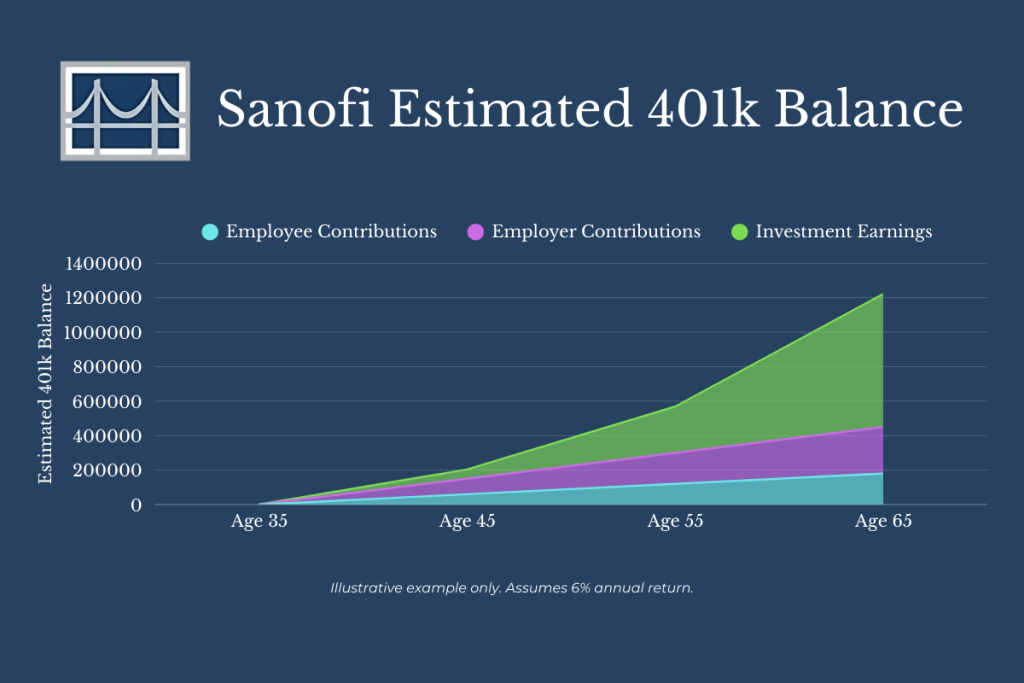

The plan provides a 150% match on the first 6 percent of pay contributed. That means if you contribute 6 percent of your salary, Sanofi contributes an additional 9 percent.

On an annual salary of $100,000, if you contribute 6% that’s $6,000/year from your paycheck and additional $9,000/year from Sanofi totaling $15,000/year. Let’s say you are 35 years old, and you keep this up until age 65. This results in a portfolio that’s around $1,200,000 with only about $180,000 of that coming from your contributions.

The remaining was from the employer match & investment earnings (assuming a 6% annual return). Now imagine you factor in an annual salary increase, or you contribute more to your 401k. This is a huge benefit for an employee.

It is also important to understand how vesting works.

Sanofi’s employer contributions are subject to a two-year cliff vesting schedule. This means you must remain employed for two years before becoming fully vested in the employer match. If you leave before that point, you may forfeit some or all of those employer contributions.

Contribution Limits and Catch-Up Contributions

Employee contributions to the Sanofi 401(k) are subject to annual IRS limits, which may change each year.

Employees age 50 and older are generally eligible to make additional catch-up contributions.

Recent rule changes have also created an enhanced catch-up opportunity for certain employees ages 60 to 63, allowing higher contributions than the standard catch-up amount. Availability depends on plan implementation, and for higher-income earners these contributions are generally required to be made on a Roth basis.

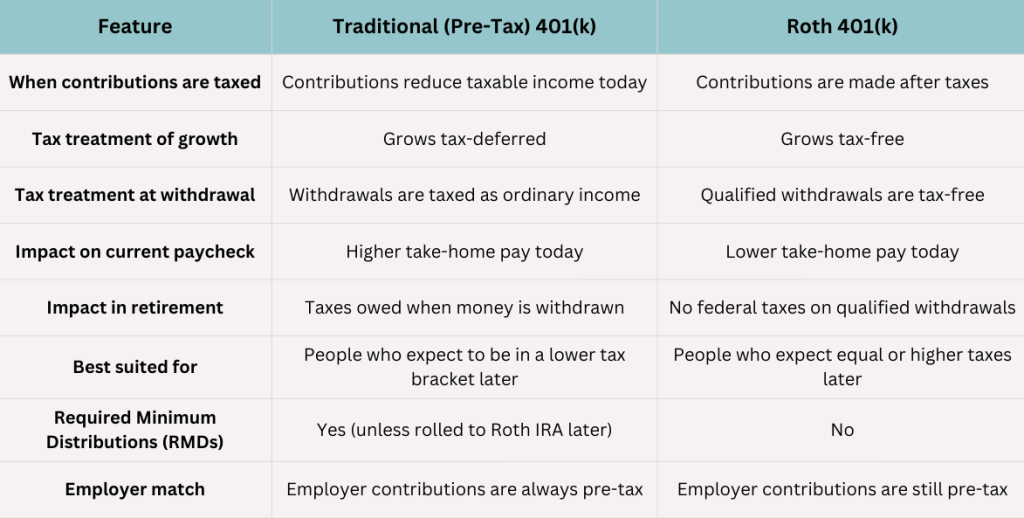

Pre-Tax vs Roth Contributions at Sanofi

One of the most important decisions inside the Sanofi 401(k) is whether to contribute on a pre-tax basis, a Roth basis, or both.

Pre-tax contributions reduce your taxable income today. Roth contributions do not. The difference is when taxes are paid.

With pre-tax contributions, taxes are paid later when money is withdrawn. With Roth contributions, taxes are paid now, and qualified withdrawals in retirement are tax-free.

Consider how your contributions align with your current income, future earning potential, and what retirement might actually look like for you.

In-Plan Roth Conversions

The Sanofi 401(k) plan also allows for in-plan Roth conversions, a feature many employees are not aware of.

An in-plan Roth conversion involves moving pre-tax money inside the 401(k) into the Roth portion of the plan. When this happens, taxes are owed on the converted amount in the year of the conversion.

For some people, this can be a way to build more tax-free income later in retirement.

For others, it may not make sense at all and could cause a huge tax bill.

Before doing this, it is best to seek professional guidance and ensure this strategy is coordinated carefully with income, taxes, and cash flow.

Investment Options Inside the Sanofi 401(k)

The Sanofi 401(k) plan offers a variety of investment options designed to support different time horizons and comfort levels with risk.

Target Date Funds

The plan includes target date retirement trusts in five-year increments. These are commonly used as default investments and automatically adjust over time. They are designed to be simple. They are not personalized.

Equity and Fixed Income Options

The plan includes U.S. and international stock funds, as well as bond and stable value options. These allow employees to build portfolios with different levels of growth and stability.

Company Stock

The plan includes a Sanofi ADR fund, though it is closed to new investments. Some employees may still hold shares from earlier contributions.

Company stock can add concentration risk. This is when you hold too much in one area that increases the risk of your overall portfolio.

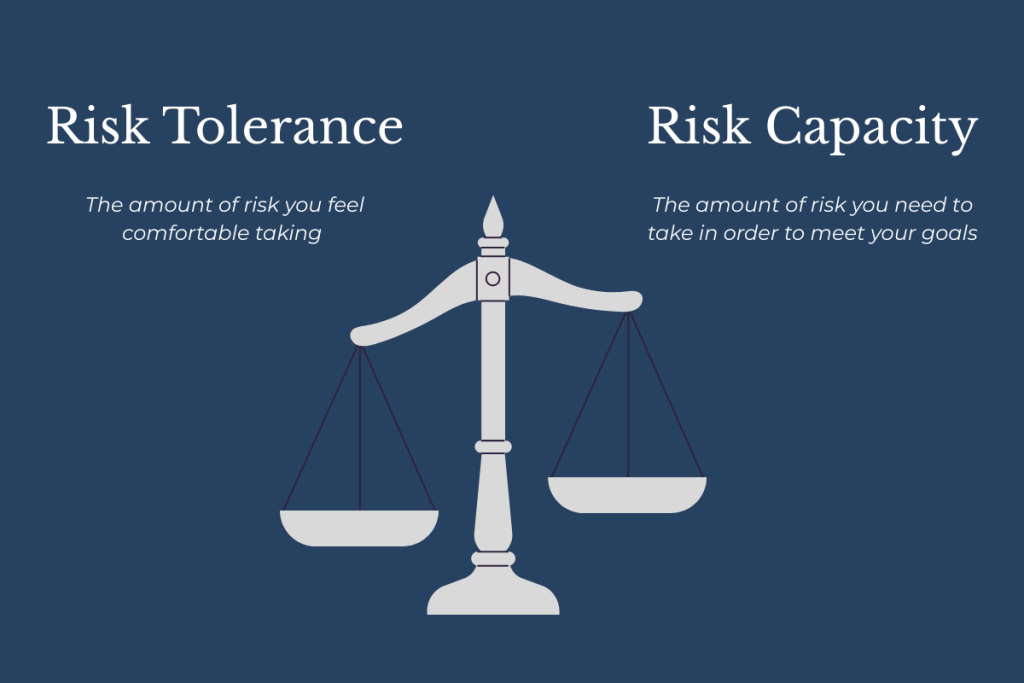

Why Risk Feels Confusing in a 401(k)

Risk is one of the hardest parts of retirement planning to translate into real life.

One term that comes up often in the financial world is risk tolerance. That is how much risk you feel comfortable taking as an individual. What gets discussed far less is risk capacity, which is how much risk you actually need to take in order to meet your goals.

Those two things are not always the same.

For example, you might see yourself as a risk taker. Maybe you love skydiving. You enjoy the adrenaline and feel comfortable with that level of risk. From a personality standpoint, we would say your risk tolerance is high.

But if you have a heart condition that makes skydiving unsafe, your capacity for risk is much lower than your tolerance. No matter how comfortable you feel, your circumstances place real limits on what makes sense.

The same idea applies to investing.

There is a difference between how much risk you feel comfortable taking and how much risk you actually need to take to support the life you want later on. A 401(k) is not about taking risk for the sake of it. It is simply a vehicle meant to help get you where you want to go.

When risk is misaligned, it often goes unnoticed for long stretches of time. Many people do not fully understand their risk tolerance until it is tested during a market decline. That is usually not the easiest moment to make thoughtful changes.

If you live in California, you know how important it is to have an evacuation plan for wildfires. It is much easier to think clearly and make decisions before there is smoke in the air. The same idea applies to investment risk.

Market downturns are a normal part of the cycle. Having a portfolio that already aligns with your comfort level makes those periods easier to navigate.

Frequently Asked Questions Aboout the Sanofi 401(k) Plan

It starts with your retirement goals. Think about the life you want and work backwards from there. Cash flow is important because you do not want to create debt, but beyond that, contributions should reflect the future you are aiming for. Simple financial planning can help you figure out the right amount.

It depends on several factors. Traditional contributions reduce your income today, which can be helpful, but they may also create a tax issue down the line. There is no one-size-fits-all rule. It depends on when you plan to retire, your other income and investments, and the bigger picture.

The main thing is overall diversification. How does your overall portfolio align with your risk and is it structured efficiently? Certain investments work best in certain accounts to reduce taxes, a concept known as asset location. It also depends on your goals and when you will need access to your money.

Income changes are a natural time to reevaluate your plan and potentially increase your savings. It is also important to consider taxes and whether this will push you into a higher bracket. Sometimes your old strategy may no longer be the most effective approach.

Your access is limited until certain ages if all your funds are in a 401(k). Truly aiming to retire early may require more accessible funds. You also need to consider taxes and how withdrawals will work at that stage. Early retirement can be a good time to start shifting some savings into tax-free accounts depending on your income. You should also consider how a market decline could affect your plan and withdrawal strategy.

Risk changes as your life changes. It is not just about age, but also your goals, timeline, and how comfortable you are with ups and downs in the market. Your risk tolerance may shift if you are saving for something short-term versus planning for retirement decades away. We have a simple risk assessment that can help determine where you fall and guide how your investments should align with your goals. Regularly reviewing your risk ensures your portfolio matches both your financial situation and your comfort level.

Coordinating the Sanofi 401(k) With the Rest of Your Life

Most complexity comes from how the plan interacts with income changes, taxes, other retirement accounts, and long-term goals.

A few examples include:

- A promotion or bonus pushes income into a higher tax bracket, but 401(k) contributions stay on autopilot.

- Variable pay like bonuses or RSUs increases taxes and affects cash flow more than expected.

- Two high earners save aggressively, only to realize all their money is locked up before age 59½.

- A long history of pre-tax contributions creates a future tax problem that was never intentionally planned for.

- Life changes, but the contribution strategy never gets revisited.

- Account balances grow, yet it’s unclear how everything fits together long term.

When Sanofi Employees Reach Out for Clarity

Most people reach out because they want to:

- Understand whether what they are doing still makes sense

- Find out if there is a better way to do it.

That usually happens around moments like:

- A job change

- A meaningful raise

- Marriage or children

- Approaching retirement

- Multiple plans across a household.

Those moments tend to surface questions.

Financial Planning Help for Sanofi Employees

At Bridgeview Capital Advisors, Inc., we help Sanofi employees translate their benefits into something understandable and usable.

We want to help you feel confident that the way your plan is set up aligns with the future you are building.

The Sanofi 401(k) is a generous and valuable benefit.

Is your plan set up to reflect where you are today and the life you want in the future?